Look, if it’s the end of the world we’re all in for a bad time. Your only hope is to be at the site of the asteroid hit at the moment of impact. Be patient zero - dying will be more fun than trying to survive the apocalypse. A financial crisis is not the apocalypse. It happens in financial markets once a decade. It sucks, but you’re not watching your family getting melted by lava.

Two things have always been true of financial crises:

- We are dreadful at predicting them.

- We recover from them.

This week, both Flipi and Ross were worried about financial or political collapse. We talk about the things within our control when it comes to our investments and those that aren’t. As any World War II survivor can tell you, when things go dreadfully politically, your wealth isn’t worth much. That doesn’t mean you should live large and wait for the end.

Flipi is concerned about a global crisis. He lives in Japan, though.

Are you guys reading/hearing or similarly being exposed to more frequent comments about another crash, correction or 'bad period'?

Would there be any preparations (perhaps even just emotionally) that people may make to ensure they don't do stupid things during such times, and perhaps come out better for it (or not worse off than everyone else) post such periods?

Weirdly, Ross has a similar question.

I have an RA with 10x investments. What would happen to my retirement should South African experience an economic collapse similar to Zimbabwe? Is there any sort of protection against this? I realize it may be an extreme scenario, but I would be nice to know what would happen.

Win of the week: Mpho almost had me in tears. This is one of my favourite emails of all time.

I have had a listening marathon of your podcast from episode 1 until the recent 101 episode and decided to finally write to you as your podcast is one of the reasons we are on this path to financial independence. I’m 33 married with 2 kids and for so long being on autopilot mode when it came to making decisions - especially money-related.

I’ve been told do well in school so I can get a job and the get married and then have x number of kids, which I did without even thinking about it.

For some reason when I turned 33 I had a freak out moment and started taking a good look at our finances. Making a combined income of around 90 000 a month life didn’t feel any different for us compared to when we had a combined income of R18 000 10 years ago. We had 4 credit cards between us with personal loans, car loans and a bond - not forgetting a R50 000 loan from my sister. I forgot about the overdraft. All these decisions were made without even thinking about it. I don’t know how we got to this point.

I started listening to your podcast and reading up on personal finance. From last year May we have paid off all the credit card debt, one overdraft and we are also ensuring that we are building up our emergency fund. We are not investing yet as focus is on building up that fund so we don’t find ourselves back in debt. The plan is to pay off all the loans, one of the cars and my sister before the end of the year.

I’m sometimes filled with regret when thinking of all the stupid money decisions we have made and how we have allowed the lifestyle creep to creep up on us without even realizing it. We now analyze our spending and have really started communicating about money, which is something we didn’t do.

We’ve cut our expenses and continue to identify areas where there is potential to cut (DSTV premium had to go). It has become a challenge to find creative ways to have fun and create memories without expensive outings and this has actually made us reach out to families and friends and spending more time with them.

I look forward to when our debt will be completely paid off and we start investing. I’m also looking forward to spending my money on things that I value and not being on autopilot when it comes to my life. Thank you for the information that you are sharing out there and will e-mail after that last bill is paid.

Josh is looking at a buy-to-let investment club

A friend invited me to join him and 2 other friends in an investment club.

He wants to set up a company for this purpose.

They want to get into buying properties.

Each member will contribute an agreed-upon amount monthly, increasing annually.

I know pooling money is a way to increase purchasing power, in this case for properties, which will be rented out.

There would also be the need to take out a bond on the property in the name of the company so I have no idea how that would work

Does this sound like a stupid idea? I know you guys are not into the whole idea of buying property, but is doing it in a club/company a better way by virtue of pooling money?

I highly recommend you watch this: https://justonelap.com/listed-property-vs-buy-let/

Wim is looking to move his RA, but Sanlam is dangling a carrot.

I am paying 2.3% in fees.

I’ve seen only 6% growth over 10 years and inflation was slightly lower.

I have to move, because my money is not moving.

Here’s a tip when you’re looking at performance over a period - compare it to the performance of the Absa MAPPS growth ETF for the same period. The MAPPS ETF has

Cash (4.48%)

Equity (72.53%)

Inflation-Linked Government Bonds (10.61%)

Nominal Government Bonds (12.38%)

This doesn’t include the 30% foreign exposure allowance in a regulation 28-compliant fund, but it should give you a sense of what a combination of assets have done over a period.

They said there’s a echo bonus being paid out in new Sanlam product.

I requested a detailed growth and cash bonus for remaining 20 years if I stay invested. Am I still getting screwed?

They promise 10% growth but have not been able to do that for 12 years. Is there a way to compare my investment in eg. sygnia RA (skeleton fund) over 20 years with this installment vs the Sanlam pie in the sky prediction?

John recently pointed out when some of these institutions promise a certain percentage growth, they mean for the period, not compounded.

Kelly is getting some first-hand experience in loss aversion.

I'm 28 with no kids, and pay R222.39 for a life policy with Discovery, valued at R751 236. I have been paying towards this for almost 3 years now. I'm not sure whether or not cancel this policy, only because that would mean losing the contributions already made. Should I continue or not?

Mike has a thought about tax on RAs.

One of the biggest issues presented with an RA is the massive tax bill due once you convert your nest egg into cash and an annuity.

If you want to access a third of your R10 million in cash, you're going to pay a whopper of an amount in tax.

However, you don't need to!

You can take the R500K in cash, tax free, and put the rest into an annuity - it's not compulsory to convert it into cash if you don't need it.

This neatly sidesteps the tax hit and gives you significantly more money to work for you in your living annuity. You'll pay tax on the income generated, but that seems fair, considering it's been growing tax-free for decades. If you've got tons of debt that needs to be paid off, then yeah, getting the cash out might be your only option, but if you've been smart about your impending retirement, then that hopefully won't be an issue.

Herman is in the process of developing a calculator that will help you once and for all find the tipping point. If he succeeds, he’ll be the Win of the Week for a whole month.

Linda is about to kick of their investment journey and wants to know which ETF we recommend. We talk about that here.

Adrian has a question about timing.

I have recently been fortunate enough to exit a business and have some cash to invest -

I haven't invested as much as I should have over the years in traditional savings but always saw my business as an asset I have been investing in.

Having sold this asset I have cash to invest but am worried about the timing of putting this all into equity markets at one point in time (markets priced quite high after a good run).

In this scenario would you do so gradually? If so, what do you recommend doing with cash as you gradually enter markets?

Ross wants to know if he’s on the right track with his ETFs.

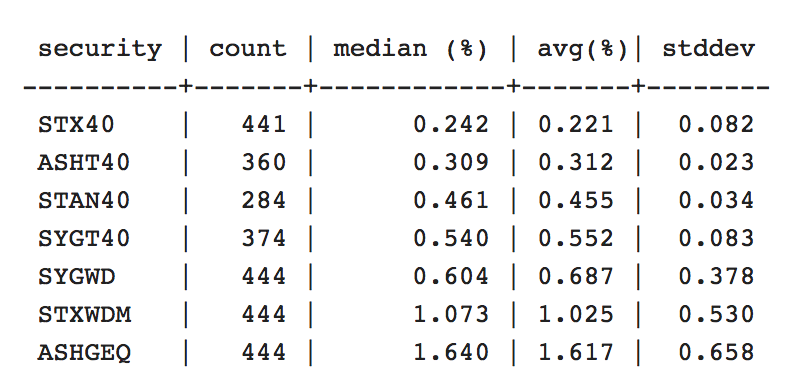

I have the FNB Tax Free Share account. I invest in two ETFs: ASHT40 & ASHMID. How does the Tax Free Shares account from FNB fair? Are the ASHT40 & ASHMID decent ETFs?

Nadia is not sure if she’s on the right track in her tax-free account.

I opened a TFSA with Easy Equities this year after doing some research and listening to your show. I've very new to the finance world so everything is a little overwhelming and confusing. I want to tell you what I am putting my money in with the TFSA and I would absolutely appreciate it so much if you could give me feedback on if you think i'm on the right track or not.

These are the "holdings" I've chosen for my TFSA:

CoreShares Top 40 Equally Weighted ETF

Satrix 40 ETF (STX40)

SYGNIA ITRIX MSCI WORLD

CoreShares PropTrax Ten ETF

CoreShares Global DivTrax

Like I mentioned, I am brand new to this game so please excuse me if I sound like a complete dumbass. (No such thing as a stupid question in this show!)

I try to keep track of what's happening in the markets but it's happening so fast, I struggle to keep up. If I had to continue my TFSA with the above mentioned, would you say I'm doing alright or do I need to refresh my choices?

Should I be splitting my TFSA money equally between the above mentioned holdings or should I be putting most of my money in the CSEW40?

Mandla has a warning about using your credit card account as a current account.

Be careful of the credit card interest free periods. A person from FNB told me that I should not be putting all my monthly debits on my credit card.

I was moving things like my monthly rent and subscriptions and recurring payments to my credit card so that I have one statement to look at each month. He says I shouldn't do this because I will get charged interest. Basically, the following transactions still bear interest:

* Cash withdrawals

* Purchase of Foreign Currency

* EFTs out of credit card account

* All transactions linked to Petro Credit card

* All budget facility transactions

I am actually sitting down to look up the terms and conditions to confirm for myself, I thought I'd just share.

I’m looking into credit card accounts myself. While there are interest-free periods, you do pay transaction fees on almost everything. A lot of people are talking to me about the rewards they earn, but nobody is saying anything about fees.

Links:

Six questions to answer before buying an ETF: https://justonelap.com/etf-six-questions-to-answer-before-buying-an-etf/

Should I consolidate my ETF portfolio: https://justonelap.com/etf-should-i-consolidate-my-etf-portfolio/

Access to a great share at a discount is something to take very seriously. Khuliso’s question about Phutuma Nathi got me thinking about BBBEE shares for the first time. I’ve never really thought about it, because I don’t qualify. However, the majority of you do qualify. How do you make a decision about whether a BBBEE share is a better investment than the ETF you would have bought anyway?

I found this conversation especially fascinating. I’m keen to hear how you incorporated BBBEE shares into your portfolio, or, if you decided against it, why that is.

Win of the week: Michael, who officially moved his TFSA from Old Mutual.

I can officially say that the transfer of TFSA money works. Haven't heard anything official from Old Mutual, but the other side of the fence seems convinced the money has arrived.

Khuliso wants to invest in the Multichoice BBBEE shares, Phutuma Nathi.

I intend on purchasing some shares when I rebalance my portfolio in the third quarter. My motivation for buy is good dividend yield. Would you recommend or be against such a plan?

How are they different from ordinary shares?

What benefits do they offer that ordinary shares don’t offer?

How should you think about them in your overall share portfolio?

Frederick has a few hundred thousand left over after selling his house, paying his debt and stashing money for his emergency fund. He’s not sure what to do.

He wants to put it in a flexi-fix deposit account with Standard Bank, and get a fixed interest rate of 8,8% per annum back. Money is guaranteed and growth is also guaranteed.

It’s always important to remember that these decisions don’t have a one-size-fits-all answer. The best course of action depends on:

- Your investment horizon.

- What you want the money to do.

If you know how long you have and you need to know exactly how much you’ll have at the end of the period, then a fixed deposit is a way to go.

If you would just like to grow it as much as possible for as long as possible, maybe an ETF is a better option.

If you don’t have anything saved for retirement, maybe you put it into an RA.

Nitesh and his wife earn a good income, but they have three kids in private schools. He wants to know what the best way is to create wealth in his situation.

John is 70. He has a fixed return investment that’s about to pay out. African Bank is offering fixed term accounts with 10.5% and 12.95% interest. He wants to know if he should be concerned about counterparty risk.

Jaco asked for some clarity on the spending ratio.

To get your spending ratio, you divide the money you put towards paying off debt or savings by your after-tax income for the month. I know it is technical, but isn't this a savings rate rather that a spending rate? If I put R15 towards savings on every R100 I am earning, I am not spending 15% but rather saving 15%? The spending ratio will be my total monthly/yearly spent against my income.

- You're right on this one!

From Manage Your Money Like a F*cking Grownup

"Take your expenses for last month. That's all the money you spent (not money you saved or used for repaying debt). Divide that by the amount you earned that month. Multiply it by 100. This number is your spending ratio.

This number is the proportion of your income you're giving away to other people and businesses. It represents the percentage of your time that you spend working for clothing companies or for your landlord, or for your bank, and not for yourself."

Soobrie is moving their TFSA to Easy Equities.

I have three years' of allocation in the tax free savings account with the Nedgroup Core Diversified fund. I'm planning on moving it into EasyEquities. Which portfolio should I choose as I can leave the money invested for another five years?

They also have 13 ETFs with etfSA and want to know if they should consolidate.

ETF: Should I consolidate my ETF portfolio?

Ben has four ETFs in his tax-free account and wants to know if he should add one for dividends.

Dividends are taxed at 20%, while you'll never pay more than 18% CGT even in the highest income bracket. For that reason dividends are awesome in a tax-free space. The real issue is, what product do you buy?

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

Interest is a strange thing, because you could at any point be earning it and paying it. In fact, if you have a credit card you could be earning and paying interest in the same bank account.

Tharina has taken steps to get her financial house in order, but she has a dilemma. She has a sum of money earning interest, and she owes a sum of money on which she is paying interest. Should she be using the one to pay off the other?

The answer can either be very easy, or very complicated. We discuss her options in this week’s episode.

Win of the week: Pieter, who has his estate planning situation on lockdown.

My wife is currently a stay at home mom. We have two kids and twins coming. There is a plan for her to go back to work at some point, but currently this is the configuration that works well for all of us.

I am contributing monthly building up a lekker EM fund. I am planning moving the entire thing into her name. I know you mentioned "What about divorce", but honestly she is not earning currently and if something happens to me she needs to be able to hold down the fort.

So our plan is as follows:

Move EM fund to her name. Currently this is just a 30 day notice deposit at FNB.

This also means she does not have to liquidate some of her assets.

It does not have to be a year’s worth of EM fund, because I have proper life insurance.

They pay a R50,000 immediate benefit within 48 hours and the rest in about 2 weeks to a month.

He also has a death letter that explains everything.

P.S. Me and my kids do not mind the swearing. I'd rather they swear and know shit.

Tharina is pretty much on top of her finances except for a car loan.

I took out a car loan. Apart from my emergency savings, I have saved a decent amount to pay off my car. It is not the total amount due. The amount is being saved in a money market account.

Would it be better to pay off my car by putting the lump sum and extra each month into the Loan Account OR would it be better to save the total amount in my money market and then settle the car loan all at once?

Johannes just got a credit card. He’s very worried about it.

I am a 21-year old student and recently upgraded my FNB account to a Gold Account which includes a credit card.

My old FNB account was an Easy account which was R5.20 p/m, but I ended up paying anything between R100 - R210 p/m for additional "services".

I decided to stop that shit and upgrade an other account which is the Gold one.

I decided to take a credit card eventually. What is the best way to use my credit card? I know a lot of people use their credit card for day to day living and pay it off at the end of the month.

I know very little about all the rules/fees that apply to a credit card. How do I use it to my benefit and hopefully save money rather than paying FNB interest each year? I hope to build a good credit score.

I know some people earn a shitload of ebucks that they use for flights etc. Please inform me best on this as well. Some people suggest to pay your salary each month into your credit card and use that...I am lost and don't want to blacklisted.

Jane has something called a “last survivor” account. She wrote back after our death episode.

My husband and I have an offshore joint and last survivor banking account. In the event of one of us dying the other one is the automatic owner of the banking account. The bank just removes the deceased spouse from the account.

We have a HSBC account. Unfortunately my local manager was retrenched and now we only have one of the expat banking services.

Isaac is 22 and has his financial situation completely under control.

- With regard to my TSFA, I have exclusively been buying property ETFs and own the Coronation property fund. Since REIT dividends do not qualify for the usual dividend exemption, the best utilisation of the tax saving would be for REIT dividends which are taxed at a person's marginal rate from the first cent. This is opposed to regular dividends, CGT and interest (first R23800 tax free). What are your thoughts on this? Am I overthinking this?

- If you sell and buy ETFs often in your TFSA, will SARS deem your intention to be revenue in nature only for ETF's in said TFSA or for all TFSA's in general? (thinking that this might be a sneaky way to day trade tax free. Not that I would day trade, but I like the thought) SARS doesn’t care what you do in your TFSA accounts. Since there’s no tax in those accounts it doesn’t matter if you trade for income or are a long-term investor.

- I own a small amount in a huge number of ETFs. Is this problem? If it is a problem, should I rebalance and incur some CGT? Remember your CGT is tied to your marginal rate, so if you want to go this route, do it now before you start earning real money. Or just pump money into preferred ETFs and leave the rest as is? (I see an IPO and can't help myself)

- With regards to Simon's comments on the three year rule and resetting base costs of investments (section 9C): The act provides this section to ensure that investors actually invest as opposed to speculate. Since it is explicit in the act, surely SARS won't penalise the taxpayer for making use of it? Eventually they'll catch on and put in an anti-avoidance provision?

Wim has two RAs and wonders if he should be moving one.

I have a Momentum RA from my employer, which is pretty much compulsory, but I have no issue with that because my employer matches my contributions.

Then I have a Sygnia RA in my personal capacity from before. Would it make more sense to move the Sygnia one to Momentum or not? Also, I feel like I am paying too much in fees. Which RA has the lowest fees? I obviously don't want to withdraw the funds due to tax. Moving them from RA a to b is tax free.

Gerhard checked out Brightrock for life insurance and he’s very pleased.

A while back I asked about life insurance and you suggested I look at Brightrock.

I have and for a product that I am comfortable provides me roughly the same as I had before I am paying R1,200 where my liberty costs were 1,650 before.

This is a massive saving.

Jacques saw a life insurance ad that promises free money. It’s a life insurance product that invests either your entire premium (if you’re under 30) or a percentage of your premium in a money market index fund. (Think TRACI). After 60 premiums you get 10% cash back.

Thanks to Londwa for sending a great video about swearing.

One of the highlights of the 100th Fat Wallet celebration was the opportunity to interview Patrick McKay about financial independence. Patrick, who runs The Investor Challenge Blog, achieved financial independence two years ago. At 39, he boasts the title of Regional Drone Coordinator and works because he enjoys it.

In this interview, Patrick tells us how he did it. He talks about his investments, how he managed to afford having a child and what he plans to do now that he can do whatever he wants.

Hopefully this is the first of many conversations with Patrick. Listen, and be inspired.

Author Sam Beckbessinger’s excellent book Manage Your Money Like a F*cking Grownup is the unofficial written summary of The Fat Wallet Show. While we didn’t know about Sam nor she about us until after the book was published, we are thrilled at the synchronicity.

She explains every principle you’ll ever need to understand to make excellent financial choices simply and understandably, sometimes even with pictures. In fact, if you never read another thing about your money, you’ll be set for life.

We couldn’t imagine a better co-host for our 100th celebration. We spoke about the one concept in her book that we’ve never dealt with on this podcast (because I didn’t know about it) - the spending ratio. As Sam explains in this episode, it’s an excellent way to measure the health of your finances, because it’s not dependent on external circumstances like the market or even your salary. You are in complete control.

To work out your spending ratio, divide how much money you put towards paying off debt or savings of any kind (including retirement and emergency fund) by your after-tax income for the month. Times that by 100 and you have the percentage of your income that you spend. Your challenge, should you choose to accept it, is to reduce that number as much as you can. The lower your spending ratio, the higher percentage of your income actually serves you.

Sam’s book also deals with the most common behavioural traps we fall into when it comes to our money. I caught myself making the most obvious one as I was reading Sam’s book - mental accounting. I caught myself before I made the mistake and saved R600! Not bad! In our conversation, she explains what mental accounting is, why we do it and how we can try to get around it.

Lastly, we talk about the final frontier in my budgeting quest. I’ve become very mindful about my money and deliberate in my savings over the past five years, but I’ve always struggled with discretionary spending. I allocate funds to certain spending categories, like groceries and petrol, but never seem to stick to that. Sam’s book finally solved that irritating problem. She explains why it can hurt being too granular in your budget.

We’re 100 episodes old*, so we might as well talk about death. Edwin is turning out to be our most philosophical user - you’ll remember him from before. This week, we help him figure out what will happen to his investments when he dies.

We know for sure every investor, trader, RA holder and homeowner will die. Why has it taken us 100 episodes to talk about the impact of death on wealth? Mostly because it’s scary and we don’t like to think about it. Estate planning is a huge part of financial management, especially for those who have already managed to accumulate some assets. It’s moving up our list of priorities in a big way. Thanks, Edwin.

*We did also smash an entire bottle of champagne while recording this episode to celebrate 100 weeks of The Fat Wallet Show. This podcast has been a transformative experience - personally, professionally and for our business. You guys surprise us with your frankness, insights and thoughtful feedback every week. You’re a constant reminder that world is full of intelligent, sincere people who care about those around them, despite what we might think after 30 minutes on Twitter. Thank you 100 times over.

You should come party with us on Wednesday to celebrate!

Win of the week: Leonora thinks we could do better in the swearing department.

Coming from the Cape, I find your swearing vocabulary very limited. A four year old down here might know more choice words than the two of you combined. 😄

Edwin has three kids and has to think about grown-up things like death.

As a 37 year old adult with 3 kids. What actually happens, step by step, to my money when I die?

I have several investments in fixed property, ETFs, unit trusts, overseas shares and a company pension fund.

I have debt in a primary home and investment home. All in all on the day of my death if I include my life policies my net worth with be positive.

I also have a will that leaves everything to my wife and kids. My wife will be richer than she was when I was alive. Don’t tell her :)

Will the bank freeze all my money until my estate is finalised? Will they take cash out of my life policies and pension to pay estate taxes?

Since my emergency fund is in my bank savings account does this mean it will be frozen too and my family can not access it?

How long does it take for an estate to be finalised? Will the proceeds from my life policies be taxed too?

Is there a clever way to plan for this so that my family can still live during the process of finalising an estate?

Is a life hack or best model for planning for this. Seems a waste to spend all of my life trying to maximize my wealth only for it to cause problems for my family when I am gone.

Njabulo is starting to see his investments work for him.

I logged into my ETFSA account for the first time since moving my contributions to Easy Equities only to find out the cash account grew by just over 66% from free money (dividends and interest). The "profit" from dividends and interest in enough to buy me another Satrix40 ETF. Small as it is, it reminded me of Lesegesha's email. Size matters very little in the world of compounding interest.

Cobus is leaving the country and not sure how to save for retirement in the meantime.

I’m 25 and have the opportunity to go work overseas. I don’t currently have plans to come back to SA. But I would like to start saving for my olden days and make compound interest works for me.

How does one go about this?

Because if one plans to emigrate, does one need to save in the destination currency?

Or buy ETF's that carries global risk instead of just SA denominated risk? Such as an SNP500 etf?

Conrad wants to contribute his full R500,000 tax-free allocation at once. Sadly, he can’t.

Karel has taken charge of his finances in a big way and was hoping we could help him with a share-picking checklist.

Since I started listening to you I’ve changed my RA from Investec to 10X.

I have opened an EasyEquities account for money left over at the end of the month that I save after cutting back on my spending.

I also managed to get rid of my bad debt and I should be able to finish paying of my house by the end of this year (done and dusted in 4 years).

I maxed out my TFSA yearly as well.

So far it’s been going great, I have bought majority ETFs and I had some shares that I transferred into my EE account.

NOW I am venturing into uncharted waters on picking my next share.

What I love about this is the order of operations. First things first - you take care of your future by taking care of your debt and sorting out how you’ll survive when you’re old. THEN you venture into the more fun stuff.

I am a sucker for a checklist.

Would it be possible for you to set up a checklist of the top 10 things to compare between companies to help me decide between say Metrofile and PSG?

All the monies I put into this account and every single share I buy, I plan to keep for the long run so good old coffee can investing.

Check out Porter’s Five Forces.

Wilhelm has questions about RA rebates.

Is the rebate to be based on your gross income?

What is the best way to calculate your tax rebate?

How does the primary rebate work?

@synapseza has such a cool money hack this week.

I have an Income Protection / Disability Protection / Life Cover/Let's-add-some-more-fucking-complicated-benefit-enhancements-and-accelerators-to-charge-even-higher-premiums product with Discovery.

The Income Protection is by far the most expensive benefit of the product. Looking through the policy document I noticed that there is a choice between waiting periods (not that it was mentioned by my broker when I signed up). I was on the shortest waiting period (7 days). But I have an emergency fund, so I really have no need to be covered for such short periods. Extending the waiting period to 30 days resulted in a 30% premium reduction (and they didn't quote for 90 days although this is an option in their product). Definitely something to check out and align with your emergency fund.

Dean wrote us about body corporate bridging solutions. We discussed this in this episode when Bronwyn’s financial advisor told her of a product with a 17% guaranteed return. Dean explains the product below:

BCBSs provide access to what would normally considered an institutional-only asset class – lending. Lending as an asset class is meant to co-exist and complement a range of other asset classes that exist in a client portfolio. It’s also important to qualify that these funds are a loan to a Body Corporate, not an investment. Our clients may view their funds as invested, but technically it’s loan. BCBSs products have the following characteristics:

Risk

- The Sectional Titles Act has protected every creditor (our clients), to the extent that there has never been loss to any creditor since the legislation was first tested in 2001, where legal precedent was set in the Amine Case.

- Legal opinions confirming creditor security include: EY Stuart, Knowles Hussain, Webber Wenztel. Contracts are drafted by Edward Nathan Sonnenberg and Werksmans, amongst others.

- We have a parking facility with Stanlib.

- Aside from the Sectional Title Security, BCBS will soon be introducing a Hollard capital guarantee on the Capital Growth Plan.

- Our cash custodian is Sanne, a FTSE 250 company.

- BCBS never touches client capital, but merely facilitates the lending process, due diligences Body Corporates and report on the capital.

- BCBS is also just the funding arm of the larger Sectional Titles Solutions (STS): (12J VCC / Solar / Outdoor Advertising / Legal / Administrative).

- Security afforded our clients, makes the product very low risk.

- A further discussion should include the lending demand of Body Corporates.

Costs

- There absolutely are costs, but none are borne by our clients.

- The borrower covers all the costs, not the lender.

- These include a lending rate, admin fees and a raising fee. (Similar to a bond application with a bank.)

- We put our clients in the position of a bank, thus there is a 0% cost implication, and a 100% capital allocation to BCBS clients.

Returns

- The very nature of a lending asset class suggests that returns are linked to the Prime lending rate.

- This is indeed the case. All BCBS’s products are linked to Prime.

- The products range between Prime + 3%, 5% & 7.5%. (Contractually specified.)

- These returns are truly meaningful, taking into account the capital security, no cost implication and the fact that Prime very rarely changes.

- Clients do not have a TER, capital is protected, there is almost no market volatility experienced.

So far, all I’ve shown are positives. As an ex-financial planner, that would make me sceptical, but BCBS clients do have negatives to contend with as well:

- The pairing of capital with a borrower does take time as there is relatively long strict due diligence process.

- As this is a loan, a client can be repaid all or part of their funds before they want the funds back. Thus they would then need to re-join the deployment queue.

- The client may also be repaid amounts that are too small to redeploy.

- Should life happen and the client needs to exit prior to the completion of a loan contract (on average three to five years), the client would experience an exit fee.

All of these items are covered in our Memorandum of Understanding and ultimately the Sale of Claims Agreement (client contract). We also encourage all clients to do their own due diligence on the products and we always gladly share any information they may require to gain a better understanding. BCBS has always been highly transparent in all areas of their products.

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

- Sign up here to receive an email every time a new show goes live.

Factor-based investing is nothing new. The idea that certain shares will give higher returns over time is the premise behind the entire asset management industry. Absa’s newish range of factor-based ETFs are as interesting for their weighting as their methodology. In this episode, we talk about whether factor-based investing has a place is passive investing.

I hate to do this to Sean, but the ABSA TFSA account has a minimum brokerage of R15, so this spreadsheet is in error, and you are still better off going with EE either way (lump sum or monthly) by a whole R34.50 per annum. That’s a free glass of wine right there!

Free wine gets you a win of the week.

Antoine discovered something in his dad’s RA that I didn’t know about. Anyone else notice this?

He wanted to know the reason for multiple endowments and investments, taking interest free loans from one and investing it in another. I confirmed with the product manager again that there are no benefits doing things this way. I believe these guys keep on lending and reinvesting the same money, because for every new investment, they generate a commission.

I explained to my dad that a R50 000 commission might sound like small change if you compare it to the final outcome of each of these investments. But consider this :

R50 000 upfront commission

Momentum borrows this against your investment at 10% interest per year for 10 years = -R79 290.00

Plus you lose a potential growth of 10% per year = R85 352,08

So the difference is R164 644,08, which means every time they generated a R50 000 commission for a new 10 year investment, with the same money, my dad is R164 644,08 poorer. There was no real value added, they probably just get their secretary to send my dad some forms to sign. It would have been better for my dad if they just took the same cash out of his pocket every time.

Thinus

If you had R10 000 per month to invest, what would be the ideal split between putting money away for retirement vs. implementing/maintaining an aggressive investment strategy?

For example, let's say this person is in their early thirties and has a healthy appetite for risk. They want to invest in the following:

Buying an RA has obvious tax benefits, but might be limited if one is seeking more risk.

Buying ETFs via a TFSA, which is obviously tax free and less risky.

And, buying single stocks (equities) either locally and/or internationally.

The responsible adult would lean more towards the RA and TFSA, but the risk-reward-seeking side of them wants to put everything in single stocks (equities).

How do you balance the risk in this scenario?

Phemelo (who was a book winner) made a difficult choice about a car.

I’ve been battling to make a decision.

We bought an SUV 2 years ago. Because service plan expires, we needed to make decision.

1.Trade in it and get smaller car

2.Surrender it to the bank

3.Extend service plan for an extra R500

4.KEEP THE CAR, SERVICE IT YOURSELF AND DRIVE IT until the WHEELS COME OFF.

We decided to go with friends’ advice to keep the car and drive it till the wheels come off. I feel I need to celebrate making this decision. Hopefully it will pay dividends in years to come.

Tshepo has a question about over-the-counter shares.

I was introduced to the word but not the research. Do you need lots of money or can an average Joe also get into it? I am looking at a company called Equity Express.

Jonathan said women with kids are excluded from the podcast because of the swearing. We asked you what you thought.

Madelyne, Ronel and Chris said they don’t like the swearing.

Tim says he doesn’t like it, but if we must he doesn’t want bleeps.

Growing up, investments weren’t often a topic of conversation. Even so, I knew that people got rich from property. I don’t ever remember someone telling me this outright. I knew for sure we weren’t the people getting rich. Still, it’s just one of those “universal truths” I absorbed as a kid.

Looking back, I realise it’s because I grew up during a property boom and a lot of people really did get rich from property. Share investments weren’t accessible or easy to understand. Financial products were sold by unscrupulous insurers who gorged themselves on the hard-earned cash of their clients. The vast majority of the population were excluded from the financial system. Property was a great way to accumulate assets and build wealth under these circumstances.

That is no longer true. The market has changed. Legislation has changed. Easier, cheaper, less risky ways of building assets are now available to everyone with a proof of residence and identification. Property is suddenly one of many ways to get rich.

In this episode, Simon and I discuss the role non-share investments can play in your portfolio. We think through two listener questions - one around S12J companies, the other, property.

Garth wants to know what we think about venture capital investments.

Since I started listening I have opened an account with Easy Equities. I’ve set up a budget, started with a financial plan, and invested in ETFs & normal shares.

My question is around Venture Capital Companies. Is it wise to buy Private equity, and get the tax relief? Or is it only for high income individuals? There is a lock in period of 5 years I see as well. This is similar to the MTN BEE shares bought a couple of years back.

I am trying to diversify my portfolio and looking at all avenues to spread the risk with the bulk being in Shares/ETF's of course.

Ros has a property investment success story.

I bought my first home - a small 3-bed townhouse in which I still live - in 1999 for R180,000 - got a loan from my dad and paid him off (including interest which he did charge me!) in two years. Then I bought a rental property in the same complex for R370,000 (including all costs of purchase) in 2004 - got a bond for R280,000 which I paid off within 3 years. I then bought a second rental property (mistake!) for R707,000 (incl. all costs) in late 2013 for which I liquidated some Satrix Top 40 and accessed the remaining capital in the existing bond, which I decided to pay off at the end of 2017. I've left the bond open and use it as my emergency fund or to help with short-term cashflow issues if a client pays me late (I'm a freelancer).

The rental income that I get from the two properties means I hardly have to work at all to cover my monthly expenses.

But with the property market currently where it is, I do agree with you that it makes no sense to buy an investment property today. The first rental property has seen capital growth of around 127% over 14 years (approx 9% pa), and then there's all of the rental income. The second property has seen capital growth of around 13% over 4 years. The two properties are of similar size in the same complex, so the difference is purely down to timing - the first was bought when property values were still going through a high-growth phase, the second when property growth had plateaued out.

We talk about this excellent JSE Power Hour presentation by Magnus de Wet in this episode.

Jonathan made the best case I ever heard for not swearing on the podcast. So good, in fact, that I’m actually considering it.

Personally I don't mind that you swear. I understand the need for creative and relaxed expression on the podcasts, which is breath of fresh air compared to radio shows.

The only problem is that it excludes mothers who have children in their cars. Yes, there are some dads that take their kids to school but invariably it’s the mom.

The result is that mothers don't end up as being financially literate in the household. As a husband, I can’t get my wife to listen to your podcast because she won't listen to the swearing. As a household, we have shared decision-making. It’s very difficult to convince my wife to listen because driving in the car is probably the only time she has to listen to the podcast.

I would very much like to improve the financial literacy of moms, especially stay-at-home moms (my wife by the way is a professional and still works) but alas, she is excluded from your otherwise excellent podcast.

I could even suggest that you take a poll in which you ask your listeners whose wives won't listen to the podcast because of the swearing and thus you could gauge from your listeners themselves.

If we are to create gender equality in financial literacy, let’s get more women involved.

- I take the point on kids in the car.

- I disagree with the view that women are more offended by the swearing than men. In fact, every email we’ve ever received about swearing has been from a man.

- That said, I’d love to hear from you on this. This show is about inclusion, which, ironically, is why we swear in the first place. We want to feel comfortable ourselves, and we want our users to feel comfortable.

Richardt let us know about a very cool tool for Sygnia investors.

Sygnia has this excel sheet which allows you to select all the funds you like on the first tab for a Reg 28 compliant investment, and then once you click Generate, on the second tab it will show you the complete breakdown of fees and total asset class allocation!

It has been updated following the budget speech.

- It’s very cool. It includes the actual rand amounts too, so you’re not just working with a percentage.

- If you contact customer service they send it to you.

Nicole is following up on the tax issue on global funds in tax-free savings.

You made a comment on having global funds in your tax free savings account.

The issue is that you pay dividend tax on dividends issued in the countries where the shares are held. The tax gets deducted from your dividends before they’re paid out to you or reinvested. If you receive dividends in a TFSA, you don’t pay local DWT, but you can’t avoid the international tax.

I have the Ashburton global 1200 and the sygnia 4th industrial revolution in mine and I'm trying to figure out if these would result in the problem you identified.

When I received local top 40 dividends last week, my offshore dividends were a line item. I hold these outside of my TFSA and I noticed that I paid local DWT on those. That’s also a line item in my statement. What we’re trying to work out is if there’s an offshore tax that was already deducted and not included as a line item in my statement. Getting an answer to this question is proving to be really hard.

Jacques has a question about his retirement tax break.

Is the 27.5% on the total pay you receive, i.e monthly salary + overtime + bonus + ......

or is it my basic cash salary before all those extras only?

My company contributes 15% of my BASIC salary (+ my 7.5%). If SARS gives us a tax break on 27.5% on total salary, that means my current contribution is much less than the "22.5%" shown on my payslip.

If I could spare enough to save the full 27.5% of my total earnings, what do I do with the extra money? Retirement annuity or Tax Free Savings account? Is there something else? HR seems to be unsure about increasing my contribution deducted directly from my pay.

Denzil wrote us in episode 94 about his Liberty RA. We made a fire under him. He also has a question about moving TFSAs.

I decided it’s time to kick these guys to the curb.

I’ve started the process to transfer my RA from Liberty into my 10X RA.

The FA was not too pleased and tried all the tricks in the book. He even then asked me who I’m moving to.

I informed him about 10X. He had no idea who they were!! I even told him about this a year ago, so much for keeping tabs on the disruptors!!

I’ve also started the process to withdraw my the other investment from them. I’ll be maxing out my Easy Eq TFSA for the year. 50% to my Emergency fund (taking it to my comfortable 6 month level). The rest will go into my Trading Easy Eq account. Again, crazy FA not happy, and has all excuses. So all is good and here's to my money actually now growing(well lets hope so!!!).

When you transfer a TFSA from one account to another TFSA Provider, do the contributions count in the year I added them, or does a transfer count for this years R33k cap?

Gerhard knows he missed the boat to win the book, but he wanted to contribute his mind-blowing financial fact anyway.

The single biggest tip I have on finances: never ever buy anything that someone is trying to sell you.

If you didn’t initiate contact the answer is always no, no matter how awesome the deal.

Saves you from being overcome by superior salesmanship and buying something you didn’t want all the way to being scammed.

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

- Sign up here to receive an email every time a new show goes live.

We spend so much time talking about bad financial products. Is there such a thing as a good financial product? If so, where would you find them?

Listener Bronwyn got badly burned with financial products in the past. She’s been paying 15% fees on an Old Mutual education policy and took out a Discovery retirement annuity that hasn’t returned anything above her contributions for the past six years. Now her financial advisor wants her to invest in Body Corporate Bridging Solutions, which apparently guarantee a return of 17.5%.

In this episode, we provide a checklist for buying financial products. When comparing similar financial products, think of the following:

- Fees

Let this be your point of departure. As winner of books and life, Ronel, explained last week, “If I get 10% growth, and inflation is 6%, there is only 4% left for growth and compounding. If I pay 3% or 4% in fees, I will only get back what I put in, adjusted for inflation.”

- Guaranteed returns far above retail bond rates

As Simon points out, the government is the only party that can realistically guarantee returns, because the government owns the printing press. You can check government retail bond rates website here.

- Counter-party risk

Investments are for the long-haul. As winner of books and real life, Lesigisha, pointed out, the principles of compounding relies on time, not money. If there’s not much information available about the company taking your money, be very careful. Counter-party risk should be considered alongside fees, though, in the case of older, bigger corporations who probably won’t go bust but happily pocket your investment returns.

- Active or passive

Simon and I spend a bit of time discussing this point. The SPIVA report indicates that actively-managed funds underperform the market year after year. However, if an actively-managed fund makes you feel more comfortable, don’t forego it just because we say so. It’s your money, after all.

Win of the week: Sean worked out if you’ll be better off at Absa or EasyEquities. He also worked out how many years it would take him to make back the penalty.

ABSA’s new inactivity cost is essentially R40.25 per every two months, but only charged five times as there would be a trade in the beginning of the year,

This adds up to R201.25 per year for the next 14 years (R2 817.50 excluding compounding or about R6 780.98 at 15% growth adjusted back with 6% inflation).

After that the fee is R241.50 per year until you remove the money, which assuming my daughter is financially savvy will be a long time as she is only 18 months old today.

Anyway before getting myself worked up about ABSA essentially stealing a month’s income from my daughter, I decided to objectively look at the numbers (boring Excel attached to check calcs) and do a comparison between EasyEquities and ABSA

For my family it’s cheaper to use the EE platform by quite a bit,

We will pay off the moving of the two ETFs in just under two years.

For someone using a monthly deposit it may be better to pay into ABSA until the TFSA allowance is maxed out and then only move to EasyEquities.

Hope this helps some peeps.

Click on the link below to download the spreadsheet.

Shout-out to Lean, who recently started listening and seems to be going through the episodes front to back. They wrote about tax on whisky, from many moons ago.

Claire wrote to say my newsletter editorial really hit her in the feels.

Your "editorial" this morning really struck a chord with me... Of course that's how they make their money. And the same goes for any of the other things we buy, oh so complicated: wine, perfume, cars, homes blah blah ~ have a great week!

Chas wants to know if we have transcripts.

I have listened to most of #96, then I was interrupted by a phone call so I lost the thread.

I am 78 and a bit deaf so I battle to keep up with your rapid delivery. Do you provide a transcript that I can study in my own time or is there a way I can pause to digest what you just said and then go on again?

I always want to learn more about investing.

Thanks for a lively intelligent show.

Transcripts are for one day when we grow up. It is our highest priority in terms of this show.

Thinus has a question about structuring his pay cheque.

When allocating your salary to different "pockets", should you use gross or nett salary?

Alexander sent this great email about selling his house.

When selling a primary residence does one pay CGT for the amount above R40,000 regardless of what you have spent on the house?

We sold our house for R50,000 less than we bought it for about four years ago.

We paid more than R500,000 towards our loan (which was mostly interest of course)

We spent about R100,000 on renovations before we moved in.

After the sale we end up with R70,000 in our pocket.

Of the R500,000 (paid into the bond) R120,000 went to the principal amount.

We sold for R50,000 less than the principal amount.

In my book, it’s a loss of R530,000 (500k + 100k -70k). Or may I only deduct the renovations? Which is still more than the 70k, but in principle can one only deduct physical improvements?

Living there cost us a fuck-ton of money.

Obviously we are getting very little out of this deal, but even if we made R600,000, I would be able to prove that it cost us much more to live there so there is no "gain".

What can I deduct from the money we get from selling a primary residence?

How does this compare to a buy-to-let property?

If you can deduct a bunch more for a buy to let, would it be worth it to buy and let to yourself?

We’ve had a few more emails from people who are upset about Absa’s fee increases. John says this is not the first time.

I bought a small amount of the Absa NewGold ETF years ago and had never done anything else with them.

They sent me a letter (in the POST) about 18 months ago telling me about a new minimum admin fee, payable quarterly. On my pretty small account it amounted to an admin fee of something retarded like 10% a year!

After querying it and getting a shrug of the shoulders, I thought FUCK THEM!! I did some research found EasyEquities, sold my ETF, was below my CGT threshold and reinvested two days later with my newly minted Easy Equities account at a newer, much higher base cost.

With EasyEquities being such a user friendly, reasonably-priced platform, I've subsequently invested multiple times what I originally had with ABSA. Their, EasyEquities’ gain.

We foolishly forgot to pick a winner for Sam Beckbessinger’s book Manage your money like a fucking grownup. Njabulo, who writes for us, snuck in his submission.

Whatever your investment or savings plan is, it is important to consider inflation and fees. If the investment can't outperform inflation after fees, that investment is making you poorer.

Jen was the Win of the Week in episode 90 for figuring out that people who don’t earn a steady income can still structure their savings by doing it by invoice paid instead of by month.

As a self-employed person without a fixed income, I can't structure a pay cheque because I don't get one. But I can apply the same methodology to each amount that I receive.

Since my last email to you about this, it has been going well (although April has been a kak month so it has not been easy).

On the odd occasion when I have been tempted to forget about my system in favour of instant gratification, I just listen to beginning of episode #90 again where you discuss my email. Straight away I am committed all over again, like I would be letting you down if I didn't stick to my guns. I know I should be motivated by how happy future me will be, but sometimes it is hard to think for two people at once.

The second brain wrinkling fact, and this isn't mine but a repeat of what you said, is the idea that our total income over a lifetime is a finite amount. Every time you spend money on something, there is something else you can't spend money on. Has that bit of information affected my spending habits!

You are changing my life and I have turned into a bit of a fanatic about all this. I am constantly annoying the crap out of everyone I know because I am trying to convert them all to The Fat Wallet Show, for their own good.

This, as well as iTunes reviews and mentioning us when you deal with any financial services provider really helps us. Thanks!

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

- Sign up here to receive an email every time a new show goes live.

This is another themed-by-serendipity episode. Last week Edwin mailed with a dilemma: how do you choose between being a good citizen or family member and having money? Whatever you spend on your family, kids or pets or donate to charity is money not going towards your savings goals. Does that mean you should forego those things altogether?

Money and morality are closely linked, but so is money and health, as Christoff pointed out. Having a lot of money but never having any fun is completely pointless. A lot of money at the expense of having children is not going to make you happy (if you want children). Sitting on a mountain of money and never helping anyone else is going to bankrupt you morally. Spending your life trying to get rich but neglecting your health is going to lead to sickness in retirement. What’s the point of that?

We discuss strategies to navigate these questions and completely fail to choose a winner for Sam Beckbessinger’s Manage Your Money Like a F*cking Grownup giveaway. Something to look forward to next week!

Win of the week: Jacques Kasselman. He found us by accident on iTunes and immediately panicked. After reading his mail I realised that he actually didn’t need to panic at all.

Where to start to get on track? I think the best thing would be to get rid of my debt of over R1500 a month, excluding interest on my vehicle loan.

I started paying off my debt by having a liberty investment I had for 6 years (R500/pm - 1.67% growth above what I put in) pay out and pay off my most expensive debt first. That's R700 that can go to the next card/account and then the next and so on.

Is this the right strategy or should I rather look for somewhere else to invest that money, eg. TFSA, ETF and slowly pay off the debt over time?

The way I understand from what I have learned from you guys so far is get rid of debt, then create an emergency fund while simultaneously slowly starting to save/invest and increasing the savings/investing part as the emergency fund gets closer to 3 months salary.

TFSAs

SARS gives us R23,800 tax free interest already. Is it still beneficial to contribute to an TFSA at possibly lower returns if we are still far from reaching that limit? Saving the R500,000 cap for when one day we pass the R23,000 limit? Reaching the R500,000 limit would take about 15 years if you contribute the max of R33,000. As I am 34, I still have 31 years left if I am unable to retire early.

PENSION

My employer requires 22.5% pension contribution monthly, deducted from my salary (me=7.5% company=15%). At the moment its split between Allan Gray and the company fund.

I plan on increasing the percentage towards retirement to max as soon as I can get the rest in order, or at least a little better.

Stefan responded to Frank, who wanted to know where to keep his Lazy system cash while he waited for entries.

I have four EasyEquities accounts and I get interest on all cash in my accounts. There’s a cash management fee, so it's not the best cash account, but it's not like I'm getting nothing.

Fred has an interesting question about TERs. He is invested in an Allan Gray Balanced Fund through a financial planner. The TER of the fund is 1.44%. In addition to that, he pays an admin fee of 0.40, an advisor fee of 0.50% and a management company fee of 0.79%. Just for the privilege of buying the fund he’s paying 1.69%.

I looked up the fund costs on the Allan Gray website, and I have some bad news. The TER is 1.45%, but excludes “other expenses” of 0.02%, VAT of 0.15%, and transaction costs of 0.07%.

3.38% total cost.

The problem is, you don’t see the TER. It costs you money, but you don’t see the money.

Pieter is putting his emergency fund to work. He banks with FNB, and he’s really made the most of that infrastructure.

- I have a cheque account that my salary gets paid in. I have a bit of extra money to cover the "shit I did not budget for". I move most of my expense money to my credit card so it is positive. This earns me a tiny bit of interest and I win back quite a lot in ebucks.

- I have a linked savings pocket with 1 months expenses in it. It earns interest, has no account fee and money is available immediately.

- I am building up 3 months living expenses in a 32 day notice account that also earns interest and has no account fee.

So the plan is: for small unplanned things, you just use money in your account. If the paw paw hits the fan I can live a month with my savings pocket money. When I start touching that money I can request "next months salary" from the 32 day notice account without incurring costs.

If I can build up > 3 months in my notice deposit, I will move that to bond ETF or something that gives better return.

This way I have no fees and costs, acceptable interest and money available now.

Gerhard needs help with life insurance.

I love your war on fees. It’s helped me a lot in making my decisions around investing.

Is there a similar type of thing in the life insurance side of the world?

My life insurance is with Liberty, and it is fully a grudge purchase, but I do have 100s of children so kind of have to have something.

Are there new style life insurance companies that you guys are aware of, like a 10X but for life insurance?

I asked the 10X team and they didn’t know of anyone.

However, I did get some suggestions.

Have a look at brightrock.co.za. It looks like a new school type of business, but it’s majority shareholder is Sanlam.

The other suggestion was FMI. They’re a division of Bidvest Life.

Craig Gradidge from Gradidge-Mahura investments said:

The insurers who are "traditional" and reasonably transparent are Sanlam, Old Mutual, Hollard, PPS. The 2 that integrate are Discovery and Momentum.

With Brightrock benefits structure is still something they need to work on...as always, the answer of which is best is usually determined by client requirements, their lifestyle and health conditions, etc etc

Poor Josh is stuck between a rock and a hard place with his RA.

I recently started working at a Big Four bank

I come from a company that used 10X as a provider. I didn't know how lucky I was back then. I am 26, so I need an aggressive portfolio.

The fund options we have are somehow administered/managed by Old Mutual and the options are:

- Allan Gray global balanced portfolio - 51% equity allocation, 1% fee on SA based assets, and performance related fees of between 0,5 and 2,5% for foreign assets. I'm staying fucking far away from this one. Assholes.

- Coronation global houseview portfolio - 49% equity allocation, looks like a fund of funds so fees on fees will apply here, but doesn't look that bad. Still shitty though.

- Investec balanced fund - 41% equity allocation, 23% bonds allocation. Fees are reasonable at 0.54% for local assets and 0.75% for international assets. I ended up choosing this one due to the lower fees, but it's so conservative, so shitty.

- Nedgroup core diversified fund - 50% equity allocation, 7% bonds. Fees are good at 0,58%. But again, lower equity exposure. Actually looking at this now, this option looks the best out of a shit bunch.

The rest are so shit they aren’t worth mentioning. Think old mutual, Tanquanta cash pooled fund (yes, seriously).

So, my question is - do I bite the bullet and just throw as much as I can at the Investec/Nedgroup funds, or maybe lower contributions to the least I can and then open a portfolio with a better RA provider like a Sygnia/10x etc in my personal capacity?

I'm leaning towards the latter. But this would probably mean some complications come tax return time? I don't suppose I can go to a massive corporate’s benefits department and tell them that my options are terrible, give me better ones?

Jorge wants to invest in a living and guaranteed annuity, but he wants to know how to make that decision.

What are the practical implications and values considerations should be taken into account when opting for both a guaranteed and living annuity?

We have an excellent article on justonelap.com/retire about the difference between these products.

Entries to win Manage your money like a fucking grownup by Sam Beckbessinger.

We asked you for the one fact that changed the way you thought about your finances.

Christoff’s point is about health.

When you realise that you need to save up for a potentially very long retirement (30+ years these days!), we do all this planning to ensure that we’re “taken care of” financially, but what about our physical health?

If we’re going to live for another 30+ years after retirement, we’d be enjoying those years a lot more if we’re fit and healthy, right up to nearly the end.

I’m 43 and take good care of myself, but I look around at my peers (school friends, cousins, colleagues, etc of the same age-group) and a LOT of them already suffer from heart problems, hypertension, cholesterol, various forms of cancer, diabetes, and what have you! It’s very depressing to think of having the benefit of living in the 21st century, with enough technology to keep us alive for so many more years, when most of those years are going to suck!

Just as compounding works for/against your finances, it does the same with our health. Poor daily habits will eventually catch up with you, so we need to keep our attention on this very important factor if we’re going to enjoy our hard-earned and cleverly-invested wealth.

Phemelo found The Fat Wallet Show in January and has made massive strides in his financial life.

I’m not all over the show.

I have a financial plan and taking on the challenge of keeping the lifestyle cost the same to avoid lifestyle creep.

My huge eye-opener was there are no shortcuts to this thing - baby steps.

I’ve closed my overdraft, I’m starting to slowly chow the credit card debt, and I started paying my student debt.

The next step is starting to slowly build the emergency fund.

Ronel had an a-ha moment about fees

If I can lower my fees on my Retirement Annuity, I can have sooo much more money.

It blew my mind that if I get 10% growth, and inflation is 6%, there is only 4% left for growth (compounding) and if I pay 3% of 4% in fees, I will only get back what I put in (adjusted for inflation). That is not my idea of a comfortable retirement ....

So I moved my Retirement Annuities from Sanlam and Old Mutual to 10X.

I am now on a fee witch hunt to cut ALL fees to the bare minimum :)

John Morrison (our retired unicorn) submitted a vote for Khuliso, I think.

When people speak about money I have realized that I must first determine their anchor point and their biases. Then I can adapt this information to my anchor point and confront my biases. Someone investing for future retirement is at a different point to another living off investments in retirement.

I am truly inspired by Khuliso and their kota. Such an understanding of compound interest, time and lowering the cost of living. Really amazing!

You can't help it if your parents were poor and you start poor, but with compound interest in a single generation everything can change. Well done Khuliso!

With ABSA's WTF new minimum brokerage fees in ETF accounts (which is by the way more than a kota) we need to get behind EasyEquities and give them huge support. Is EE the only company that understands not to rip off the poor?

Links to be included in show notes:

Adam sent a link about the three biggest lies about passive investments.

They are:

- People can’t make their own decisions about which products to buy

-

- Very few investors have the time, knowledge or skill to invest their own money.

-

- The fees aren’t as low as they claim

-

- Passive products available to retail investors in South Africa are still relatively expensive and not that much lower than actively managed funds.

-

- You don’t get market return

- It is easy to compare the JSE/FTSE All Share Index returns with active manager returns and conclude that active managers are not worth their fees. The comparison is flawed. It does not consider risk and it also does not take into account that most of the growth from that index has come from one share – Naspers.

I’m not going to tell you what to think about this. If you understand how these products work, you can make up your own mind.

If you secretly hate us but haven’t been able to find a different source of financial information, I have some great news! I found a Freakonomics Radio episode that summed up exactly the principles we champion on this show.

In this episode, Simon and I take the financial literacy survey. It’s only three questions, but understanding their answers will enable you to make great financial decisions. If this sounds vaguely familiar, you might be thinking of this podcast we did last year.

Here are the questions:

- Suppose you have R100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow?

- More than R102

- Exactly R102

- Less than R102

- Imagine that the interest rate on your savings account was 5% per year and inflation was 6% per year. After one year, how much would you be able to buy with the money in this account?

- More than today.

- Exactly the same as today.

- Less than today.

- Do you think the following statement is true or false: buying a single company stock usually provides a safer return than a collective investment scheme like an ETF or unit trust.

Win of the week: Rob has been coming to our events for ages. He has some ETF investments, but he’s been wanting to trade since the day I met him. This week, he sent this email:

Yes I have done my first trade and bought my first bunch of shares (7 shares in total - some bits and bobs) (as oppose to ETFs)

I am not sure how I am supposed to feel!

Its bit like sex for the first time - did not know what to expect!

Frederick

My world has been turned upside down! I started listening to your podcast a week or so ago, and fok... my google is broken!! From googling sport all day I now spend endless nights and have sleepless nights on where to put my money and avoid tax as much as possible!

I use to think money is money and my RA is perfect and that life is sorted! I was wrong!

I have an RA (diversified wealth builder) with Sanlam. Any thoughts here please? My FEES (to my knowledge) is 0.65%.

It says “management fee at benchmark %”.

I put some money in monthly with a 10% annual increase. By retirement I should be paid out R11,5m.

Let’s say you live another lifetime after your working life, how much will you need? It’s possible to retire at 60 and live to 100.

https://justonelap.com/podcast-much-money-need/

Frank is trading Simon's Lazy system and wants to know if he can park his money somewhere while he waits for entries. He’s not earning interest on the money that he’s allocated for this trade.

Shamona wants to know if timeshare is worth it.

What are the pros and cons? What should I look out for when buying?

Entries to win Manage Your Money Like a Fucking Grownup. We want you to share the financial fact that blew your mind. We’ll be running this competition for one more week.

I asked author Sam Beckbessinger hers and she said on R10k per month, you’ll earn R19m in your working life. Mine is that a low cost of living is basically the answer to all your problems.

Lesigisha wrote back after we sent him a shout-out last week.

Thank you so much for the great affirmation I received from the submission of my email, it really really went a long way in validating what I’m doing.

It’s hard to start on this journey, but after doing it for a while one does sometimes get despondent and wonder if this is worth it. Your affirmation has helped reinvigorate me and I go back to it every time someone says they’re waiting until they have a bigger shoe size before they can start making “real money decisions”.

Khuliso’s mind-blowing fact is that you don’t need huge amounts of money to invest. As a result of his mail I spent a lot of time thinking about kotas this morning.

The most mind-blowing fact was finding out that if I can afford to buy a kota (R23.00) or street wise 2 I can afford to invest in the JSE and create wealth.

Even though it's little money, over the long term it makes a difference. In my case the problem was lack of information rather than a lack of money to invest.

I am now very conscious about my spending habits. Whenever I buy takeaways in the back of my mind I keep on thinking of ETFs that I could be buying. When I look back, I see missed opportunities where I could have invested and build wealth.

It’s becoming increasingly clear that access to money isn’t always the best thing. In last week’s episode, Pieter explained how access to a free house and investments didn’t make him great at money. Fat Wallet bestie and newly appointed spy, Wilhelm, sent us news from the front line this week.

Wilhelm started sorting out his money and sharing his journey with us when he was still a student. It’s been such a pleasure witnessing his pre-income journey. If you can figure out your money situation before you actually have any, how much you earn becomes irrelevant. You’ll be a financial success.

Sadly, the opposite is also true. I certainly learned that the hard way getting into mountains of debt in my 20s. The difference between me and Wilhelm’s new colleagues is that I earned a junior journalist’s salary (basically just enough to make my engineering friends feel sorry for me). The amount of damage I could do to my financial life was artificially limited by the amount of money I earned. Thank goodness.

This week we talk about the dangers lurking behind the piles of money of high-income earners. If you’re a low-income earner, this is good news for you too. These are the traps to watch out for before the dineros start rolling in.

We are giving away a prize for the first time ever. Sam Beckbessinger is the author of Manage Your Money Like a Fucking Grownup. She donated a copy of her book to one lucky Fat Wallet listener. Find out how to win it in this week’s show. You can find out more about the book here.

Kris

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

- Sign up here to receive an email every time a new show goes live.

Wilhelm writes:

The government takes really good care of its young doctors. We get a good salary, but the lack of financial education means that a lot of that money simply gets wasted.

I know of three doctors living in my building who purchased expensive brand new cars (Mercedes Benz A class AMG, Audi RS3) before receiving their first salary (and without receiving any help from their parents). They bought cars on credit using only a contract from the department as collateral, where it has often happened that people do not get paid the first month due to the poor admin/payroll/HR abilities of the DoH. One is paying an interest of 13% over seven years.

In PE we get the opportunity to live in the doctors’ quarters. It’s an old apartment building in an old and rather dodgy part of town, but it is centrally located with adequate security, a brilliant sea view. We get to live here for R1100 per month. My flatmate and I pay R2200 for a three-bedroom apartment.

Many of the new doctors don’t want to live in the flats. They are old, the outside looks a little dilapidated and the first two floors had a history of cockroach problems (which has been sorted out). They justify their choice with, “I’m only here for two years, I’d rather live close to the beach.” They pay between R6,000 and R8,000 per month for two- or three-bedroom apartments. This often excludes water and prepaid electricity or 24-hour security. That is 300-400% more than we are paying.

The last thing I noticed is the absolute ignorance towards savings and investments. Of the 52 interns who started at Livingstone hospital, I’ve chatted to more than 40 of them and only two of us have TFSAs.

One of them even said his financial advisor told him that TFSAs are “only for poor people”. People blindly follow the advice from advisors from companies like Sanlam (which gets sold to us under the Abacon brand), Old Mutual and Liberty with very few people even knowing that 10X, Sygnia and EasyEquities exist.

People have private financial advisors that have them investing in Funds with TER > 3% with many hidden costs. When they asked them about TFSAs, they said “oh yes we can talk about those when you want to get serious about saving!”

From a financial point of view I’m on target to have my TFSA topped up for 2018 within four months. My emergency fund is also growing nicely, already up to three months of living expenses.

I’ve also done a bit of research and found that you can save quite a few rand every month on insurance if you increase your excess payments when you claim. You should only do this if your emergency fund is able to cover the amount of excess that you are taking on (maybe even two or three times over so that one single claim does not consume your entire emergency fund).

Mary-Ann wants to know if her emergency fund can do better.

I am currently keeping my emergency cash funds of about R100k in my OST account which currently earns me 5.638% - better than a Savings account.

I’ve been trying to figure out if it is worth putting that cash into something like the Newfunds GOVI ETF or Newfunds or Satrix ILBI ETFs.

It seems to me like I could earn closer to 8% there although would need to deduct the TER from that return.

I realise that the capital could fluctuate slightly, but is there significant capital risk to make it not worthwhile? It could get liquidated if required in a few days. I would probably continue to keep a portion as cash for immediate emergencies that could not wait a few days.

What are your thoughts on pros and cons of this strategy? Where might I do better? I hate having money laying around not earning its keep!