Diversification is an important part of risk management in a portfolio. Unfortunately, as with all things finance, there’s no simple diversification solution. This week, we address two diversification concerns: being too diversified and not being diversified enough.

Diversification is an important part of risk management in a portfolio. Unfortunately, as with all things finance, there’s no simple diversification solution. This week, we address two diversification concerns: being too diversified and not being diversified enough.

In my own portfolio, I pay attention to three diversification criteria, namely assets, regions and sectors. Since I want my portfolio to grow as much as possible, I prefer equities as an asset class. I don’t diversify this much, since I understand the risks involved and I have enough time to recover from market events.

To diversify across regions, I choose equity-only investment products that invest in multiple regions. ETFs with world-wide exposure are excellent vehicles for regional diversification.

In terms of sectoral diversification, I prefer investment products that invest in sectors relative to their importance in the overall market at the moment. I do this by avoiding sector-specific investments.

My single ETF strategy also takes care of my diversification needs. When I can no longer afford single asset class exposure, I’ll have to start including assets that are less risky. For now, one ETF rules them all.

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

Bhiri

Can it be wrong to be too diversified?

My portfolio is probably made up of 75/25 between ETFs and pure direct shares. The 25% shares I am not worried about as, as I get older this percentage will only get smaller and most of my investments will be in ETFs. I'm 37 now. I have the ASHT40, GIVRES, STXIND, S&P500, STXNDQ, SYGWD ETFs and also the STXPRO and SYGLB in my TFSA.

Stefan

I was doing some housekeeping on my two ETF portfolios. I ran a report on all dividends received in the 2018 calendar year.

Even though my PTXTEN from a capital appreciation perspective is deep in the red, I was really happy with the total div received compared to all the other ETFs in my portfolio.

My other property ETFs are not performing as well. For example CoreShares S&P Global Prop did about 50% of what my ptx 10 did.

Which other ETFs have a similar yield? I would like to diversify and buy more etfs but with yield in mind for this particular portfolio. I’d also prefer etfs that are more geared towards global exposure. It doesn’t have to be property.

Matthew

I have taken a more active approach to my TFSA and am now sorting out my TFSA with EasyEquites.

Now that I have gained the confidence to self manage my TFSA, I am wondering if I should do the same with my RAs?

Between a Retirement Annuity (RA) and a Tax Free Savings Account (TFSA), which should be prioritised?

Is managing your own Retirement Annuity through a site like EasyEquities a viable option?

I noticed the RAs have fact sheets and it feels similar to TFSA. The fees are also under one percent which is way cheaper than with my current provider.

Do I have to take into account Reg 28 when I am investing on the platform? I currently assume all available options are all Reg 28 compliant and I can just invest where I desire.

Are there any investment strategies with regards to a RA? I am only away of appropriate risk e.g. high risk early and move to low risk near retirement.

Could a RA be seen as an alternative to life insurance (assuming living annuity)?

E.g. Take life insurance for the first 5 years of your working life and after that, cancel the life insurance as the RA will pay out to beneficiaries to an equivalent life insurance?

RAs will pay out on serious ill-health / Disability. Is this not an income protector or are there scenarios where an income protector would still be needed as the RA will not cover? Also, would you even recommend an income protector?

Jonathan

My mother, who moved overseas, sold her primary residence.

She has around R1.4m sitting in cash. She is 55 years old, has just enough money to live off from alternative income. Listening to your show, buying another property to rent out seems like a bad idea.

She has a place to stay and enough money to live off. She would like to know what is the best thing to do with the money as she grew up thinking buying property is the only good thing to do with large sums of cash.

Karabo

10x is relatively new and my friend asked what would happen to the monies invested with the fund manager should they go bust.

Is there a way we can "insure" our investments against funds managers going down.

Cliff

I have a few debit orders with EE and I want to be sure that when buying on those predetermined monthly dates I am not penalised by buying at inflated prices (when market maker is offline). How would you suggest I go about this?

Nerina pointed out the cost of debit orders.

Steve

If we ask our financial adviser to drop his fees - and rather pay for his/her time - what rate is reasonable? And how much time per year ?

I have only a basic RA and basic cover (disability / income protection) - under the financial advisor’s care. I doubt it’s more than 2-3 hours per year?

For my actual meetings with my adviser I am paying close to 20k per year - last five years are hardly beating cash - with a pricey platform (AG).

Don’t want to be insulting but short of cancelling and moving to 10x I thought I would offer to pay per hour and see if anything changes?

Doug

My wife and I max out our TFSAs and have been for the last two years.

I have a pension fund through my work which is relatively fixed. My wife works for herself so, based on advice at the time, opened up an Allan Gray (bleh, fees) Unit Trust. We have ceased contributing to the fund but are unsure of what to do with the amount sitting there (approximately R120k). We have a home loan and are well ahead of curve there - likely to be paid off in about 10 years or so.

What do we do with the R120K?

One option was plowing it all into the home loan to reduce our debt. That would sure feel great but then our only retirement savings would be our TFSAs and my pension fund from work. This feels a bit light and the R120k was initially set aside as part of a retirement investment plan.

The second option we considered was putting this amount into some low cost ETFs on easy equities as a discretionary investment.

The third option was some sort of a split (80/20) between ETFs and the home loan.

Is there something else I am missing?

With the potential of kids in the future we are unsure of our ability to push as aggressively into investing or the loan.

I’ve only ever known debt as the wrathful destroyer of wealth and happiness. Lately, however, I’ve come to realise debt can be a powerful tool in your financial arsenal - if you treat it with respect. Someone recently explained the logic behind maxing out his child’s tax-free account instead of saving for her education.

I’ve only ever known debt as the wrathful destroyer of wealth and happiness. Lately, however, I’ve come to realise debt can be a powerful tool in your financial arsenal - if you treat it with respect. Someone recently explained the logic behind maxing out his child’s tax-free account instead of saving for her education.

If a single year’s tax-free contribution can cover much of your child’s living expenses in retirement, imagine what 15 years’ worth can do. Giving a tax-free account time to grow will have greater benefits in the long run than if she started contributing when she started working. Instead, she can use her starter salary to pay back low-interest study debt with her retirement taken care of. It’s genius.

This conversation got me wondering whether I’m making the most of the debt I have available. My home loan is currently the dumping ground for all my savings. This brings down my repayment period and guarantees a higher interest rate on cash savings than any bank can offer me. In this episode we discuss how low interest debt instruments like student loans and home loans can be used to inch us forward financially. We discuss why cars and clothing accounts won’t form part of this strategy and try to figure out when a credit card can help.

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

Alexander

My studies are financed by my parents’ home loan that has an interest rate of 9%. This interest rate is still currently better than student loan interest rates I could obtain (10%+). The idea is that I’ll start to repay my parents as soon as I start working. I calculated that I’d most likely graduate with R350,000 to R400,000 student debt owed to my parents.

Should I use the very little free cash I have from my monthly allowance, vacation work and mentoring remuneration to:

- Contribute to my all-ETF TFSA at EasyEquities?

or

- Contribute to my savings account with TymeBank (at a 10% interest rate) to pay off my student debts sooner when I graduate?

I know the amounts I’m investing/saving now might be insignificant relative to the massive amount of student debt. But I’d still like to know what is better: investing in your TFSA or attacking student loan debt as soon as possible?

Clarke

My wife and I are in the process of finalising plans to build our dream home. We’ve saved up about 50% of the funds required, which is sitting in a money market account.

We hope to get close to 90% building loan from the bank which would enable us to use very little of our own cash in the initial stages of the build. Hopefully we can pour that money into the loan as required in order to keep interest payments to a minimum while having access to the bond if required.

I’m currently working on an exact schedule of cash flows, but I would require to draw down our investment periodically over the next 7-9 months in order to keep the loan amount to a minimum.

Which investment would you advise I could look into apart from money market accounts or fixed deposits that might yield greater returns without substantial additional risk?

Siphathisile

When I did my articles 2017-2019, I went to the SARS website and answered questions to see if I need to file a tax return. The website said I didn't need to, I'm guessing because I earned too little. Now that I am a qualified professional I know I will have to and I have no clue where to begin...stories about long queues at the SARS offices make me keep procrastinating on going there.

My company offered to pay half my medical aid. Should this affect my PAYE tax amount? Am I paying tax on my gross amount or on my (Gross plus medical benefits) ? I asking because the difference in the amount is nearly R500 and that hurts.

Am I liable to pay UIF since I am not a permanent resident and I am not a citizen of south africa? Will I be able to claim if I was ever unemployed in South Africa?

Shaunton

Do you think it would be more beneficial to add more contributions to my RA or do you think I must open an easy equities ETF account if I want to save more over and above my TFSA and RA?

Steve shared an excellent article.

- Reduce your tax bill in the current tax year

- Reduce your tax bill in the next tax year or in future tax years (any unused portion carries over indefinitely)

- Reduce your tax bill when you withdraw or retire from a retirement fund

- Help you to get tax back from SARS on your living annuity income when you file your tax return

- Reduce the tax bill on cash your beneficiaries may choose to take from your retirement fund or living annuity on your death

Francois has an idea for a calculator to work out how much money you have left until you die.

It should show you how your savings grow on a daily basis!

So what must it do?

- You tell it how old you are and when is your birthday.

- You tell it to what age more or less you intend living. 8, 90,100

- You tell it what your balance is of all your money and assets.

It then works out how many days are left from your current day to that age and it calculates how much money you can spend per day up to that age. If you don't spend any money today, tomorrow your daily spend automatically increases since you did not spend anything today or you received interest overnight or whatever.

You see your balance grow NOT monthly, but daily! Later you add on expenditures and it automatically calculates your new daily balance and so on.

MacGyver

I have a TFSA through FNB. I max it out every year, it's the first money I put away.

However, it sits in cash in this FNB TSFA. How do I go about transferring this to Easy Equities Tax Free account so that I may invest in ETFs instead of it simply sitting in cash in my FNB account?

Register here to attend Stealthy Wealth’s meet-ups.

I learned a lot of important financial concepts from the FIRE (financially independent, retire early) movement. The most useful is the difference between retirement and financial independence.

I learned a lot of important financial concepts from the FIRE (financially independent, retire early) movement. The most useful is the difference between retirement and financial independence.

The days of companies supporting retired employees in retirement are a distant memory. If you are plugged in to your finances, this is great news. It means there’s no correlation between your age and how long you have to work. We focus instead on financial independence.

All of us have a magic money number. The great news is that our number is entirely in our control, because it’s based on our spending. Simply put, your monthly spending times 300 gets you in the ballpark of your FIRE number.

That formula works because of the 4% rule, which our friend Stealthy Wealth lays out in this post. Basically, 4% is how much of your portfolio you should be able to cash in every year to allow your capital to grow by inflation. That means your portfolio never shrinks, so you never run out of money.

If you accept the 4% rule, you have to reject some age-old ideas about asset allocation as you approach retirement. In retirement planning, we are often advised to deduct our current age from 100 or 120, depending on what you suspect about your longevity. The number remaining is the percentage of your portfolio that should be in equity. Unfortunately that means a person who is 50 years old will have half their portfolio in low risk, low growth assets.

The 4% rule is unlikely to apply to such a conservative portfolio, since it’s unlikely to yield high enough above-inflation returns. Remember, you can only use whatever you earn above inflation to keep your capital in tact. If inflation is 6% and your portfolio only grows at 7%, you can only use 1% of your capital. Unless you have a huge amount of money, that won’t be enough to sustain you for a year.

In this podcast, we brainstorm new ways to think about how to set up a portfolio as you approach financial independence. We work on the premise that you need between five and 10 years’ worth of living expenses in low-risk assets on day one, so you have the option of not drawing down your portfolio during a market crash.

We offer more questions than solutions in this one. We are excited to hear what you have contribute.

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

Colin

I signed up for a Just One Lap's ETF portfolio subscription account over two years ago and have been using the recommendation for my TFSA. There are supposed to be subscription fees payable after the first free year, but I have never been approached to pay any fees to keep my subscription account active and my login still works!

I am concerned however that the portfolios I see when logged in are perhaps not the most current, because I have not paid subscription fees! This concern is brought about by comments I have heard on the Fat Wallet podcasts, that make me wonder whether the current > 10 year portfolio (that has holdings: CSEW40 40%, SYGWD 40%, PTXTEN 20%) is the current recommended portfolio. For example Simon often mentions on the podcast that the Signia MCSI World ETF have much higher costs that the Satrix equivalent, and given Just One Lap's emphasis on watching and reducing costs where possible, that makes me wonder why the SYGWD is still in the >10 year portfolio and whether I am seeing updated portfolios.

Margaret

The recent discussions about CoreShares changing their index made me want understand more of the underlying methodology of the underlying index.

Indices for one country seem relatively simple (e.g. S&P 500, our Top 40 index), but if you want to go for the one ETF to rule them all strategy you have to have more complexity. I see there's the Ashburton 1200 and the MSCI world that track the global markets. Could you explain how these indices are created?

Are there any indexes that track emerging markets over the world? BRICS? Latin America and Africa?

Kristia’s ETF analysis checklist:

- Asset classes: are you buying shares, bonds, property or a combination?

- Regional exposure: where the companies in the index operate

- The investment universe: is it the whole market or only a sub-sector of the market, like technology

- Methodology: how the index is weighted.

- Sector exposure: what types of companies are in the idex

- Cost: at the moment TER is the most universal indicator

Philip

A financial adviser suggested we take out life insurance on our parents as a future investment. My parents agreed and I have a little under R5m cover for about R2750 p/m.

The policy is now eight years old and the payment amount only adjusts for inflation. So does the payout.

- a) It's my understanding that I will not pay tax on this payout.

- b) I hope I don't lose my dear mother for the next 30 years! And even if she lives until 90, my calculation is that the contribution will never exceed the payout.

To me this seems like a good investment as part of a bigger portfolio (RA in addition to my Work pension, Standard Securities -started trading on the lazy system {yay me! I'm a trader!} etc).

Are there any pitfalls I am missing, or can I tell my sister to consider the same type of policy?

I guess I just want a sanity check here.

NC van Heerden

Over the past year I’ve listened to all of your podcasts since inception-sometimes obsessively. Luckily I started listening only a year after I started working before I had the time to make poor financial decisions. Following the great advice you have been giving, I have:

- Started a maxing my TFSA which I spilt 70/30 between STXWDM and STXEMG

- I have created a sizeable emergency fund, which already saved me on one occasion

- Started some discretionary investments in the ETF space

- Moved my RA from a advisor-fee stacked unit trust to 10X. I’ve stopped contributing to this fund to keep the opportunity to move overseas without Mr SARS having his cut – these funds are currently going into my discretionary investment (thank you to everyone who did all those calculations about if the RA vs discretionary)

I currently have a contract until the end of 2019. Thereafter there is a high possibility of hopefully only a few months of (f)unemployment. At that time I am hoping to cover my expenses by working as a locum while waiting for a post to open up. Luckily I have no debts – thank you just one lap.

In preparation I want to try saving a bit more money into my emergency fund this year. I’m currently using FNB’s money maximizer account (decent-ish) interest rates but 100k minimum and monthly fees, but it has easy access via the FNB app (which I use anyway) and I can move money immediately).

Since I will be adding some more money into my emergency fund I was looking at at saving it somewhere with a better interest rate. According to tigersonagoldenleash.co.za at the moment the best interest rate seems to come from Tyme Bank (10% after invested for more than three months and taking a 10 day notice on withdrawal – downside is a maximum investment of 100K).

Does that seem sustainable on business grounds? I always have the uncomfortable feeling that something seems too good to be true (looking at you Absa with 13.5 percent interest and then fine printing it as simple interest). I’m also considering African bank as it seems a bit more established.

Please also advise if you think there would be a better place to park some extra emergency fund money for the next few months.

Rudolph

Do dividend yields rise or fall in a boom or a recession?

Hannes

You’ve mentioned a few times already that buying your house was a mistake and you'd never do it again. I would love for you to elaborate exactly the reasons why you believe it was a mistake, in as much detail as you can.

I find it difficult to believe its a financial mistake when you are planning on paying it off in five-ish years, paying very little interest because of that, and having the benefit of not having a rent / bond payment after said five years. To me the pros of this far outweigh the cons.

I apologise to Four Cousins for saying they probably add bubbles using a SodaStream machine. I've learned my lesson and vow to buy a bottle should I see one in store.

Investing in listed companies is a great way to learn about investment risk. It teaches us that sometimes the market isn’t rewarding at all and that individual shares can do better or worse than the average. We also accept that bad market periods are generally followed by periods of growth. We develop respect for the fact that no company operates in a vacuum. The economy is a complex system that can impact the performance of individual companies in surprising ways. We learn all of this while also thinking about the companies or products we invest in. We have to keep it in mind, because we are stock market participants from the moment we buy a single share.

When it comes to unlisted investments, the risks change. The biggest risk is not being able to find a buyer for the investment. In addition to providing a secondary market to buy and sell shares, the stock exchange requires a degree of due diligence from companies, adding a further layer of security. While unlisted companies can be good investments, it can be hard to keep track of the market in which they operate, to be sure that they comply with the law and to get truthful information at regular intervals.

The case of the Highveld Syndication Scheme that Liezl invested in is a great example of the types of risks we take in an unlisted environment. While the company initially operated legitimately and offered great returns, a management change resulted in great losses for investors. Was there any way for an individual to predict this change? Unlikely.

In this episode we discuss some options when you’ve made a bad investment. We talk about some of the risks of unlisted investments and how to know when to get out.

Read more about the Highveld Syndication Scheme here.

Liezl

I invested in the Highveld Syndication Scheme (HS22) when I was still young and dumb.

We opted for a settlement arrangement a couple of years back to get at least 55% of our initial capital back over a 3-year period. That did not materialise.

In the beginning of March we received a letter offering us APF (Accelerated Property Fund) shares to the value of 25% of our initial capital amount as a final settlement by Nic Georgiou.

The catch (of course there is one) is the shares are offered at NAV price (R7.50) and not market value which is around R3.40. The highest ever price recorded in 2016 was just under R7.00

A second catch is the CEO of APF being Michael Georgiou.

I also believe the share price will even drop further once these shares are allocated and everyone hits the sell button on day 1.

One tiny silver lining is the anticipated opening of the Fourways Mall this year which forms part of the property portfolio.

I'm thinking of just taking the settlement, get it over with and play a bit of monopoly?

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

Win of the week: Jonathan

Thank you for such an incredible podcast. I feel on top of my financial life, and it is truly because of the idea of "don't get financial advice, get financial education". I'm happy to say that your podcast has been the cornerstone of my financial education and continues to reinforce the principles that I need to focus on.

This question is something I've wanted to ask you for a long time. You always say we don't talk about Japan, and it truly is the single area which I feel you and Simon fail your listeners in. One of the most important financial principles is to confront the truth and then deal with it. Basically, I think you owe it to your listeners to TALK ABOUT JAPAN.

This video sent by Dhiraj explains a bit of the economics of Japan.

Mike

We bought a townhouse and were lucky enough to afford to keep it when we bought a house when we had our kids.

While it has appreciated 40% in value in the six years we've owned it, beating SA equity markets over the time, it's been pretty flat the last two years.

I am wondering whether we should sell it, settle the bond (we don't pay any tax on net rental income yet), and invest the R1m or so we'll have left after fees into low-cost ETFs.

The property is located in a great suburb, but it's only 1km from our current house, so I worry about concentration risk.

The net yield after all costs is also not great at around 6% based on current market value (9% on original purchase price), but what's nagging me is that at some point the property market must bottom out and Newlands would be one of the first areas to start growing well above inflation again.

Brecht

I’ve had a Momentum RA policy since 2002. The fees are 2%. The penalties on a R160,000 policy are R30,000 if I want to move to another provider. Do I move this fund or just stick it out because of the high penalty? My thinking is I will make that loss back and some more if I can move this fund to a better growth product and less fees?

I’ve had a Discovery RA for the last 10 years. It has only brought me growth of 1.89% pa and the fees are in the range of 2.5% - 3%. I am expecting a fee payback in April which will at least boost it a little, but the returns will still be shocking. On top of this I have 2 other preservation funds with Discovery that have done around 6.5% pa respectively over the last 10 years. What shocked me even more is that 60% of my combined Discovery portfolio is in cash. I haven't found out the penalty cost of moving the RA as yet but definitely need to move them and especially into a more Equity driven fund.

Is it possible to combine the two RAs into one fund?

Is it possible to move different preservation funds into one and is it wise to that?

Brandon

Are there rigorous studies (literature) available that address your premise that advisors add approximately zero value. I'm asking because it seems logical to me that your conclusion rests on that premise being true.

My concern is that if there were say, a number of comprehensive global studies that arrived at the opposite conclusion, would that not have a significant impact on the financial advice that you deliver on your platform? Are there global studies that examine the question, do advisors add so called alpha -- put simply, would an average individual working alongside a professional competent advisor, outperform that same individual, operating on their own in a parallel universe.

If it were true that the net effect (after fees) of working with an advisor were positive, the compounding arguments you make in your podcasts would work in precisely the opposite direction.

We mention the SPIVA reports, the Morningstar research, as well as the Berkshire Hathaway newsletter: Berkshire Hathaway letter on fees

Theo doesn’t agree that a home is just a lifestyle asset.

When staying in a paid up home you are not paying rent, so your paid up property is saving you the equivalent rental. It is indeed an asset, although you are not earning a yield you are saving opportunity cost of paying rent. The rent also increases every year which makes the benefit of owning your own asset even more beneficial.

Sandile

Heading into 2019 I've set serious objectives around how manage my money, which has been a lovely journey so far. I've become the biggest cheapskate, focusing all my efforts on saving as much as possible.

My next step is building a long-term investment strategy, I've received pricing from my advisor. I am beginning to question every piece of his advice due to the insurance matter. He is suggesting I invest in Allan Gray Balanced fund and Coronation Balanced Fund. Last year he recommended Allan Gray and the Investec opportunity fund.

I have looked at each fund in detail and the confusing element is 1) fees and structure. For someone who is new to the game it definitely is overwhelming. 2) Most of these fund invest in the same companies?

I'd also like to invest in ETF funds but I see there a plenty options to choose from.

Bruno

Would it make sense to duplicate the same investment strategy for both of us in a TFSA? In other words, purchase the same ETFs for both of us.

Money is inextricably linked to every aspect of our lives. Every milestone and setback is either helped or hindered by our financial situation. When we plan for life events like weddings, babies, retirement or death, we also think about their financial impact.

Money is inextricably linked to every aspect of our lives. Every milestone and setback is either helped or hindered by our financial situation. When we plan for life events like weddings, babies, retirement or death, we also think about their financial impact.

Most of us fall short in planning for things we don’t like thinking about. When our nightmares become a reality, the last thing we want to worry about is money. This is normally what insurance is for. Sadly the insurance industry is a flakey ally.

In this week’s show, we discuss the financial impact of debilitating sickness. We talk about the preparations you should think about when you’re healthy, as well as some options for people who are already dealing with this difficult reality.

Louis

Over the last couple of years I went from buying a new, heavily financed car every one or two years, to (almost) owning one car for four years and the other for 10+ years.

I scaled down after parting ways with a major client. I decided to pay off all debt except my house. I saved the R8,000 I would have paid on my car each month and in 2.5 years had the money earning interest in my bond. I started investing in the stock market and also have a number of ETFs, including a CoreShares tax free account that actually gave me a good return over the last three years.

We adopted at the ripe young age of 45, which changed my outlook on money. My wife was diagnosed with MS last year. Suddenly all the insurance policies and annuities became important as we had to become a single income family.

We took out a combined policy with life cover and LIVING LIFESTYLE COVER (with all the PLUSES, which Liberty say they gave us for free). According to what my current broker and I could deduct - upon diagnosis we should receive 25% of our insured value.

This is not the case, though. Liberty has their own definition of MS and you should tick a number of boxes. Even though my wife had several problems relating to MS, we were not entitled to any payment. Not once did Liberty make contact with my wife’s neurologist, doctor or anyone else.

My wife had a relapse during the year. At first Liberty again refused any claim without making contact with anyone. Eventually they paid 25% according to their sliding scale. Now that my wife stopped working, I’ve had to employ a neurologist to advise me in order to decide on further action.

In our situation we will survive on my income, taking into account retirement provision might be a problem. What do other people do when the sole breadwinner is in the same situation?

Secondly I checked the annuity we have been paying for the last 15+ years and realised that the return was just over 6% for the period after cost.

The obvious thing to do was to cancel, for which the charge is 5%. They say that after 15 years they have not recovered all their cost. There is a contribution charge of 4.5% and then they charge a management fee of almost 2% on top of that.

I wrote to the pension fund adjudicator and after waiting almost seven months and requesting feedback a number of times, I received feedback basically saying they can charge up to 20%. I am moving the money in any case as I am sure we will be able to do better somewhere else. R14,000 on a R280,000 value. If you deduct the R14,000 my real growth over the period is probably very close to 0%.

What is the best fund with a moderate to high risk to try and make up for lost years? We already have investments in Allan Gray Balanced and similar funds.

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

Gareth

The problem with dread disease cover is the companies’ definitions of their sicknesses. I unfortunately had the same claim disappointment when my wife was diagnosed with Crohn’s disease, I then only found out that they pay out 25% of the dread disease assured amount. The same goes for MS and most autoimmune diseases.

We pay discovery R12,000 pm on the top Medical aid so they can pay R30,000pm for her medicine.

Liberty should’ve asked for medical reports etc from the doctor as part of the claim process.

I always say that dread disease is a nice to have, same as capital disability, but the most important benefit to have is income protection. The income protection doesn’t look at your illness but more at your ability to do your specified occupation. It is more expensive but will pay out in a lot more cases.

Win of the week: Riani, who is 13, and her sister Juané, who is 7. Their mom tells me they already know what the ALSI is.

Brendon

I’m able to invest R15,000 a month. Should I go down the ETF or individual share route? Do I incorporate property ETFs too? Should I open an EasyEquities account or with another company?

Steve

I’m still left wondering what to buy, especially for my TFSA. There just doesn’t seem to be any right or wrong answer?

All things considered, what would be your preferences if you wanted exposure to the following:

US Markets?

World Market - Developed?

World Market - Developed & Emerging?

South Africa?

My understanding is that the US leads the world economy so what are the chances of their markets slowing down while the rest of the world starts ticking? If that’s unlikely, surely one could just as well stick with the US?

Donal

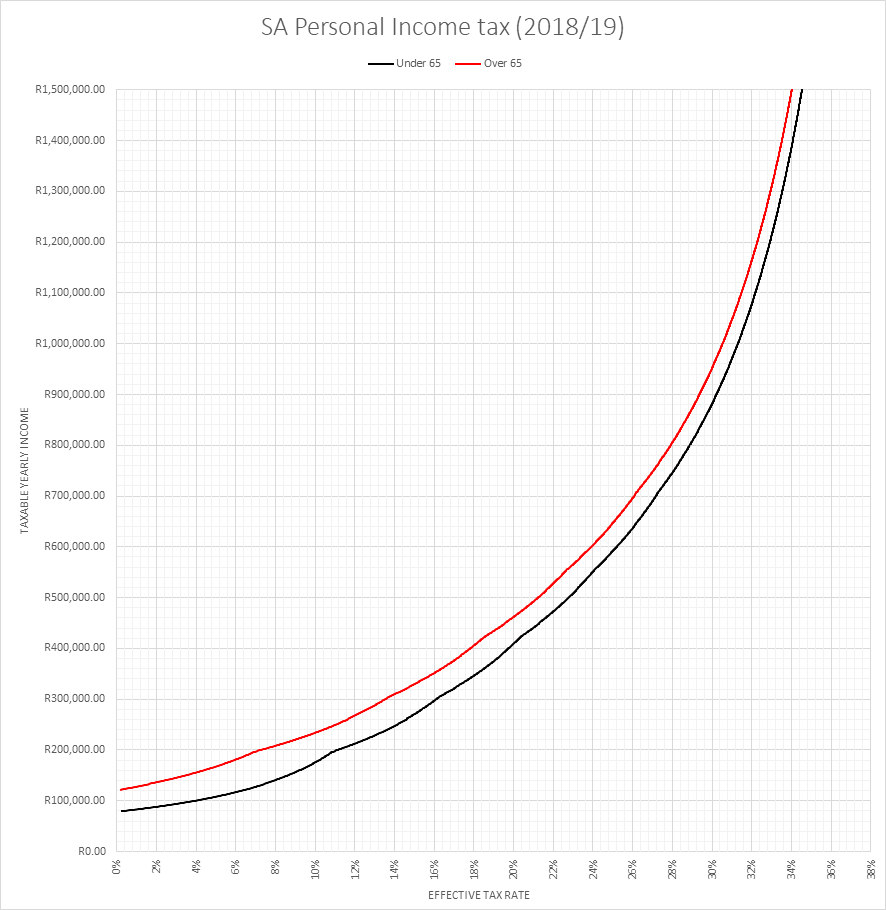

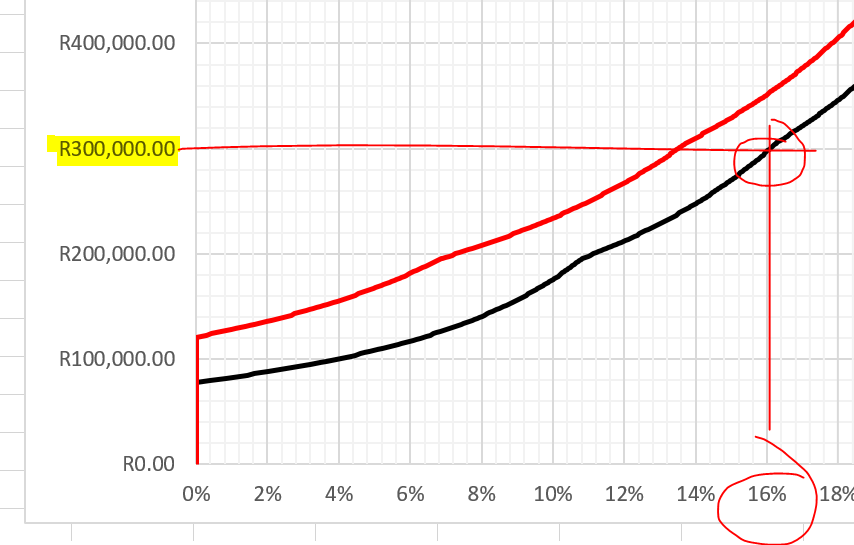

I did a spreadsheet to work out the tax for the two scenarios and I then backtracked and worked out the present value. There's not a huge difference. The tax man would get almost the same amount of tax from me eventually even if I leave the pension alone!

I've listened to you guys saying many times we should clear our debt as fast as possible.

I currently have a large car loan at prime + 0.9%. I change my car approx every 2.5 years. In that time I'll generally only have paid off half the loan. My trade-in value usually just covers the outstanding amount and then I need to get a new loan for the full value of the next car and the cycle starts all over again.

I commute to work and drive approx 1,000km per week. So after 2.5 years I've clocked up around 120,000km. That's around the time that things start to go pear-shaped with a car.

I could pay extra into the loan and reduce the capital quicker. Let's say, for example, instead of paying into my TFSA I put R2750 per month into my car loan. So, like I do, I've run a spreadsheet and I've found that after 18 months (which is when I will change again) my capital balance will be R60k less than if I didn't pay in the extra. So the loan on my next car will be R60k better off. This sounds great, but the problem then is that my TFSA capital doesn't grow! And if I continue to do this every time I buy a car I'll then my TFSA will always suffer.

Eventually I'll be in the situation where my initial loan amount will be small enough that I'll be able to pay off my car loan before I have to change my car again. In that period I can catch up on savings for a few months. But I reckon it's going to take about five more car changes to get to that stage! By then I would almost have my TFSA maxed to R500k and I should be sitting back with my feet up watching it grow and grow!

The thought of not investing in my TFSA for the next 10 years is extremely painful and seems to be counter-intuitive. But should I just suck it up and rather focus on clearing my car loan every month?

Sabata

You guys were slagging retirement annuities as if they are lepers! Any unused contributions to an RA can be carried forward, which you mentioned somewhat unconvincingly.

This is not a 'small benefit', as you stated. These unclaimed contributions can be carried forward all the way to retirement. By then you probably won't be investing for retirement. You can use these to increase your tax-free lump sum you're allowed to withdraw, or to reduce the tax payable during retirement.

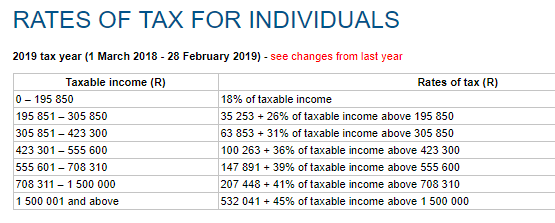

Say you retire with R 50,000 per month. Tax payable would be R 12,582.25 per month. Let's say you have enough unclaimed contributions banked. You could then claim your 27.5% of taxable income as an RA contribution. This would reduce your taxable income to R 36,250 even though you will no longer be making these contributions. Your tax would be R 7,521.25, a saving of R 5,061 per month! That's worth a lot of bubbles, especially if you drink Four Cousins!

About your diplomat who is based in Botswana, is she exempt from RSA tax because she is out of the country for more than 183 days, or is it because of her occupation? I think it's the former.

Rieneke

I have a slightly different take on the issue. Use life cover as life cover when you need it, but change the purpose to inheritance when you no longer need it.

You often take out life cover with a young family as you have to provide for them should something happen to you. As the kids then leave home or you no longer have dependants, the life cover is cancelled. Especially older folks who might no longer be able to afford the cover. In that case, offer it to your children as an investment. You have low premiums, having started young.

Taking it out with the purpose of inheritance when you're older is too expensive and taking it out with this purpose when you're young is also expensive due to time and as your fortunes change, might also not be able to sustain it, in which case it was wasted.

Ros

I'm keen to move my emergency fund from a Money Market account to TymeBank. This seems like a no-brainer - If I understand their Ts & Cs correctly, once your money had been in a GoalSave account for 90 days, you get 10% interest for a 10-day notice period, up to a maximum of R100 000.

I mentioned this to my Mom and she was very concerned that the bank could go under, a-la African Bank or VBS. What are your thoughts on this?

Stealthy Wealth’s FIRE-people are organising get-togethers in Durban, Cape Town and Port Elizabeth. Find out more here.

When you’re just starting out on your investment journey, dividends seem like much ado about nothing. That’s because dividends get paid per share. If you don’t have many of those, dividend amounts can be laughably small. It’s hard to get excited about R25.

When you’re just starting out on your investment journey, dividends seem like much ado about nothing. That’s because dividends get paid per share. If you don’t have many of those, dividend amounts can be laughably small. It’s hard to get excited about R25.

However, long-time rich-ass shareholders will tell you dividends become way more fun the longer you invest. It’s a good idea to have your dividend strategy in place while you’re only getting a R25 twice a year. In this episode, we share some options for your dividends.

Sheldon from Twitter

When looking to invest in equity with the aim of receiving dividends. How much should the price action influence your decision? I.e. if price action is bearish/flat but the equity pays decent dividends, how does one ensure they don't lose money.

Morore from The Fat Wallet Community

What is the best strategy for reinvesting dividends within a TFSA? Do you reinvest in the ETF that paid out? Do you use the dividends to buy the cheapest ETF at the time within your portfolio? To keep the "right" balance, do you reinvest them in terms of your predetermined allocation strategy?

Caroline

I was using the strategies above, but then I decided to reinvest the dividends back into the ETFs that earned them to get a better idea of the ETFs overall performance.

Win of the week: Gerard has a tip on avoiding the huge spreads on EasyEquities.

On the Buy screen where you fill in the amount you want to buy, click on "What's been happening to STX40 in the market".

This will show you a graph, and three prices - Last Price, Selling At, Buying At. You want to make sure your Last Price and Buying At price are close together. If Buying At is much more expensive than Last Price, then odds are the Market Maker is offline, and you should rather come back later and try again.

EasyEquities is not a perfect system, but it is cheaper than most... just don't get burnt with this annoying thing.

Tash

I had an opportunity to work in Germany and have been here since 2012 on a temporary residence permit.

I'm on the compulsory pension system and have an RA to squeeze the tax man back. I plan to be here for the long run, but home is where the heart is and I would want to spend lots of time in South Africa when I retire.

I’ve opened a TFSA with EasyEquities in 2018, because we don't have such a wow savings initiative in Germany. Here the tax man does his best to grab deep into your wallet at every opportunity.

That said I want to have a long-term savings plan in South Africa. German interest rates are laughable and the savings plans are even worse. I listened to Simon's recent lecture at the JSE and one of the first things he explained about the TFSA is that you have to be a South African resident. The term “South African resident” is coming under scrutiny with the new emigration laws.

Will my TFSA be valid and inviolable if I remain a South African citizen, with a residential address ?

I maxed out my 2018 contribution and plan to do the same till I hit the R500,000 limit.

What implications are there for a TFSA if you spend most of your time outside South Africa and your main income is earned in Germany?

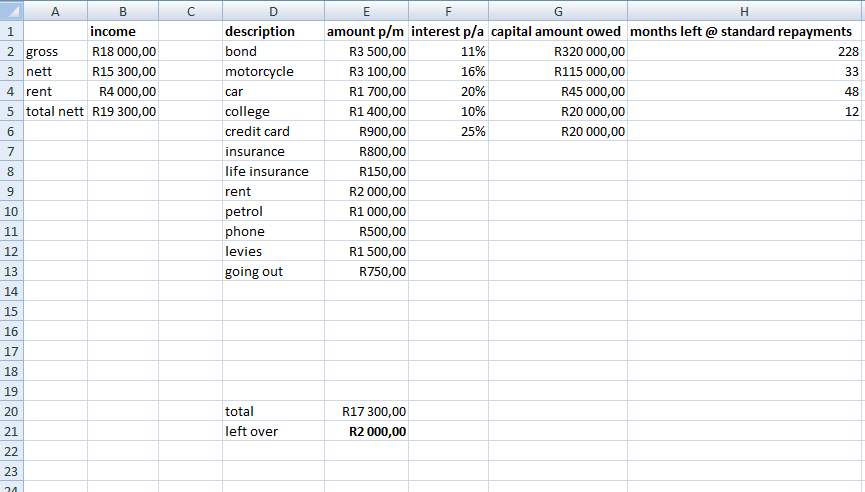

The Bank’s Cash Cow

I’ve gotten myself into a debt hole, and it’s completely my own fault.

I'm trying to figure out which one I should pay off first, and if i should consider debt rescue.

I thought I should pay off credit card, then motorcycle, then college, then car.

Gerard

I watched a lot of Simon's trading videos in 2016. I wasn't planning on trading, just thought I might learn some stuff. Using Simon's Lazy System, I back-tested some of the things I hold, and the signals there are pretty clear for when to sell. It probably would've have meant that 2018 would've been a positive year for my TFSA.

In one or two of the videos Simon states that when he hits 100K in his TFSA, he will start trading in the Tax free account.

I'm now interested in starting to trade my TFSA, but there is an alarm bell going off in my head:

Why does Simon, who is an experienced trader, not trading his TFSA and recommending that it's probably better not to ?

Sarah

If you want to sell some of your shares, to the precise degree that you can get R40,000 of capital gains in a year, and no more: How do you know how many shares to sell?

The online platforms will give you a form AFTER 28 Feb telling you how much capital gains you had on that year’s sales, but that is too late to inform your selling decision.

In Cape Town, rental prices on average increase by 10% per year. House prices (excluding the Atlantic seaboard) increase at more like 6%. What does this mean for rental prices 10 or 20 years from now? Does it mean that renting will become inhibitive at some point? Do you think the market will balance itself?

You mention that moving in a bit early and paying occupational rent before the transfer goes through. Can you explain a bit more why that would be a beneficial thing to do? My guess is that if you move in a month or so before the transfer goes through and you discover things like leaks, cockroaches, etc. it will be too late to change the terms of sale at that point anyway, due to the ‘voetstoots’ understanding.

The tax-free investment case is so appealing, it’s almost always a good idea to do your tax-free investing before anything else. Even fancy algorithms like this one finds that. Sadly, life happens to our money and a full tax-free allocation isn’t always possible.

The tax-free investment case is so appealing, it’s almost always a good idea to do your tax-free investing before anything else. Even fancy algorithms like this one finds that. Sadly, life happens to our money and a full tax-free allocation isn’t always possible.

This week, we help a father of four figure out how to balance his educational priorities with his tax-free allocations. The good news is there’s no one right answer. You have many options, including pausing your tax-free contributions and taking it up again later, as Njabulo pointed out in this podcast. The bad news is sometimes two options have more or less the same benefits and shortcomings. In that case, it’s time for the soft sciences.

I always talk about the importance of knowing what you want your money to do. Since Tinus chose to have four children, we can assume his family and children are his top priority. His finances should reflect that. Secondly, a great education will empower his children and offer them a greater likelihood of being financially secure themselves. Tax-free is important, but it’s not the be all and end all.

Tinus

I try to max the contributions for myself, my wife and my four kids every year, even if it means I need to sell from my existing portfolio to get the required cash.

I hope that I’ll be able to teach my children enough about finances that they’ll handle their TFSAs with care once they turn 18.

My initial idea was that they would pay for their own studies from the TFSA, but it would probably not be very smart to start withdrawing from the TFSA as the real opportunity of compound growth is just massive if they can keep the investment going.

Projecting the value of a maximum annual contribution up to the R500,000 level and 8% annual return, the account at age of 18 would sit at around R1.2m. This R1.2m becomes R31m by the age of 60, which should allow them a comfortable retirement from the TFSA alone.

Surely this “asset” in the child’s balance sheet would make getting a study loan much easier if required, especially if the TFSA is then moved to a provider that also give study loans (type of a soft security).

How do you balance the contributions made to your child’s TFSA and provide for their studies? I’m leaning towards maxing out the TFSA and face the music to pay for studies when the time comes.

I have always believed in choosing stocks with good momentum. For this reason, I initially chose the Satrix Momentum Unit Trust for two of my children’s TFSAs and I’ve been contributing to them all along with TFSAs at Satrix directly.

I noticed that there is now a Satrix Momentum ETF, that seems to be exactly the same as the unit trust, just lower cost. ABSA NewFunds also have a momentum-based ETF. I am considering moving these two kids TFSAs over to EasyEquities for easier admin and future flexibility, but would like to stick to a momentum type fund for now. How do these options compare (the methodologies are not the same as is evident from the current holdings in each fund).

For my two youngest children I chose the Sygnia 4th industrial fund (mainly because it sounded cool and I thought choosing technology for my 0 and two-year-old can’t be a bad idea).

Their investments have done very well (just lucky timing to be honest). From your recent podcast I could pick up that you are not a massive fan of this fund (it invests in guns etc) and I know that there are performance fees as well. What would be other options in the technology space, just a simple Nasdaq ETF?

Find our house view on tech ETFs here.

Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

- Sign up here to receive an email every time a new show goes live.

Win of the week is Hannes for sharing a great car financing tip.

For anyone interested in calculating car affordability (because some of us love cars and it’s also our hobby, not just a means of transport), Dave Ramsey has a cool rule stating that you can afford the car ONLY if you can tick off all three of the following:

- You are able to pay a minimum of 20% deposit on the car.

- You are able to finance it for a maximum of four years (48 months).

- The monthly repayment (after 20% deposit and a max four-year term) is less than or equal to 10% of your gross monthly salary.

I've done the math like this and it removes a lot of the thinking involved in buying a car, especially if you're a petrolhead. Use it / don't use it. :)

Alistair

I received my very first dividend from my Ashburton 1200 in my TFSA today (yay), but I was quite shocked to see I paid 26.76% tax.

That seems like an extremely high price to pay for a tax free account - I was under the impression it would be much lower. I do know we are subject to foreign dividend tax, but considering this is how much tax one is paying... is it even efficient to put ETFs like the Ashburton 1200 in a TFSA? Surely (if your finances allowed it) it would be significantly better to fill your tax free with local ETFs and all foreign ones outside of it? Or is the advantage of not having to pay capital gains tax so great that it completely out-shadows the tax on dividends (and the growth that taxed amount would have had)?

I'm curious what difference this tax would make over a period of 40 years, conservatively assuming the growth of the Ashburton 1200 was the same as that of the Satrix 40 (and assuming dividends are reinvested).

Anne

I have an offshore investment with Allan Gray. The money split between Orbis Sicav global balanced fund and Nedgroup Investments Core Global fund.

I wanted to make an additional contribution, and had a relook at the fees. TER 1.08 and admin fee of 0.5%.

It the investment worth the fees? Should I rather stick to ETF in EasyEquities?

Ned inherited R2m.

With such a large amount of money, the fear of investing is damn real. My biggest fear is that I find myself fiddling around with my money until I find myself in a “ah fuck” situation. As a result, I have over R1.9m just sitting in cash. I realise this is a bad thing and I plan to move it all to EasyEquities, minus the emergency fund.

The real fear comes in with my discretionary investments.

I’m 29 and a major career improvement is imminent if all goes well. This will bring with it a MASSIVE change in salary. The plan is to continue dumping all my excess salary into tax free and thereafter discretionary investments. I’m not too sure about an RA at this stage as this is something else I’ve been putting off.

The only real investments I have outside of the tax free are about R18k in Ashburton 1200, top 40 and mid cap ETFs through FNB which I’ve been contributing to since about 2014/15.

Investment fear is a very real, very scary thing. It just gets worse when there’s more money. I realise now how important it is to start early and when you don’t have so much money to stress over. I wish more people would realise that investing isn’t only for rich people. It’s the best thing you can do for yourself.

John

In SA we have the Top 40, so an equal weight equates to 2.5% per share. Our biggest share is Naspers which is about 22.5% of the index, so Naspers is 9 times bigger than the equal weight. (22.5 divided by 2.5)

In the USA they have the S&P500 so an equal weight is 0.2% per share. The biggest share is Apple which is about 3.6% of the index, so Apple is 18 times bigger than the equal weight. On a relative basis Apple is twice as concentrated as compared to Naspers in our market.

Now I am guessing but I believe most of the data to validate the equal weight model has come from the USA and not from SA. This could mean the the equal weight model is not effective in SA.

When the expects say "over the long term shares have outperformed the other asset classes" I guess that they use the the overall index to validate their statement. I guess they are not referring to some bespoke index with smart beta components. To me any "smart or not so smart beta" is moving away from passive investing towards active investing even if the costs are lower. Passive investing should be no more complicated than reproducing the index.

Is it cheaper for CoreShares to change the methodology of an ETF compared to launching a brand new ETF with a different methodology? My guess is that it is.

I believe that CoreShares must stick with their model or front up and tell the market their model is broken.

Martin

I am a 26-year-old Mountain Guide living in Somerset West. I have a wife and a one 1.5 year old little girl dinosaur. My wife doesn’t work.

I am busy studying and I hate traffic so I leave home at 04:30 most mornings to avoid traffic to Cape Town where I then have 1.5 hours to listen to your shows and do other studies while I wait for my clients to arrive. I finish work at 11:00 and can spend most of the rest of the day with my wife and daughter.

Recently I started my own business and make a reasonable income during the summer months and then eat only putu in winter.

I save a fair amount of my income, mostly because we live very basic with no debt.

Anyway my questions are the following:

I don’t plan on living in South Africa for very long, another four years, at most. What impact will this have on my TFSA? Will I be able to keep it growing and fill it while we travel? I don’t plan on emigrating anywhere, so my bank accounts should stay in SA for the moment.

Would it be smart to start investing in a RA if I’m not going to be in SA. Can I transfer my RA across borders later in life?

I know you did that blog post on the global property ETF, but I was wondering if that is a good investment into my TFSA? I thought I will only get tax exemption on local property like the satrix property ETF. Will I get dividends on those two global ETFs? What Property ETFs should I be looking at?

This is not the first time I’ve heard people buying insurance products to leave money to loved ones who aren’t financially dependent. In cases of premature death, it’s genius (aside from the dying). However, insurance companies are money printing machines because they understand how to harness probability.

This is not the first time I’ve heard people buying insurance products to leave money to loved ones who aren’t financially dependent. In cases of premature death, it’s genius (aside from the dying). However, insurance companies are money printing machines because they understand how to harness probability.

When you take out a life insurance policy, the insurance company works out how many years of contributions they’re likely to get from you before you hop off your mortal coil. They do with your money what you should be doing with it - they invest it. They understand money today is worth more than money tomorrow. If this didn’t work, the insurance industry would not exist.

Lady Kabelo is thinking about life insurance.

It would only be to give my folks, my sister and my partner a nice lump sum when I die, not because they depend on me financially.

I just feel tired of black people dying poor, leaving relatives to scrounge to bury us. I want to leave them with money to bury me and then mourn with bubbles or, if they listen to me, put the lump sum in a retirement fund for future comfort.

You could argue that I should invest that money and they will inherit that. But if I die next year, it wouldn't have grown to a considerable amount. Life insurance would pay out a nice amount between the four of them.

Is my thought process as crazy as I think it sounds, or would this fall into the category of making your money align to your values? I love my people and if I can put some money aside now so they get some money when I die, why not?

Win of the week: Cheryl from The Fat Wallet Community.

Nedbank offers a Greenbacks shop card which allows you to draw your Greenback value in cash from any Nedbank ATM. You could then use this cash to buy your bubbles. I draw mine once a year in December and use this money towards Christmas. I try to get Christmas for free - using Dischem, PnPay points and greenbacks to pay for gifts and christmas lunch shopping. Not 100% achieved but getting closer every year.

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

Jacob

I have a debt problem that I need to address, but my wife is not helping. She is also in debt and her business is not making enough money. How do I convince her to start a financial plan so that we can address our debt problem in order to be able to buy a house?

Gerhard

Just listened to Simon’s JSE direct around the changes in CSEW40.

The question I was waiting for but that never came, is what will the impact be on the TER of the ETF if they make the change.

It doesn’t help they smooth the ride, but in the end you lose because of fees.

Bella

I had been investing R500 per month with Discovery Retirement Optimiser Endowment policy for the past 10 years. It grew by 13% in that time.

To say disappointed is an understatement, seeing that I’m just 10 years away from retirement age.

I’ve decided to take the plunge and invest in ETFs with the proceeds from my unit trusts and endowment policy.

I’ve recently transferred my RA to etfSA and also opened a tax-free account. I’m contributing R1500 p.m towards Coreshares Global Dividend Aristocrat, Coreshares S&P 500, Satrix Emerging Market, Ashburton Global 1200.

Should I open up a discretionary account (with EasyEquities perhaps)? I’m looking at offshore ETFs but unsure on what that spread of the funds should look like.

I also have an investment property but my tenant has lost his job and is paying a lot less than the amount I’m asking for, and I’m not sure for how long he will even be able to keep this up for.

Should I just consider selling and investing these proceeds as well?

Martinus

My 14-year old car said its final goodbye and had to get a new car sooner than I expected. I only had 50% of the cash on hand to purchase the new car, then I had to to either take out a loan for the reminder, or take money out of my TFSA or a paid up RA. I figured the wiser choice was the loan since drawing from the capital of a TFSA so early hamstrings your future growth.

Considering a high interest car loan, would it be wiser over the long term (20+ years) to put that R2750 pm that would go to a TFSA to paying down the loan and then miss out on the TFSA allotment for a year?

My math shows that if I pay an additional R2500 a month on my car loan I'd pay it off 21 months early, saving me R24150 in interest and R1449 in fees.

I'm leaning towards paying off the loan, because it’s the first time in my life I have debt and I really don't like it.

Boitomelo the Diplomat

I am looking at increasing my RA contribution. I started with a low amount 2 years ago. I’ve read that 27.5% is the maximum tax benefit I can get towards my annual RA contribution. Is this 27.5% of my contributions to the RA, or of my taxable income? If it’s based on my taxable income, how does a person in my position determine what my maximum RA contribution would be since I do not pay income tax?

Secondly, given that my contracts will expire in 6.5 years and that I’ll be without formal employment, is increasing an RA a good idea given that I’ll only access it at 55? It leaves me with an 11-year access gap. I will be looking for a job and other alternative sources of creating income, one of which will be to provide editing and French translation services which I can’t currently do.

I know that freelancing is not easy and that one should be sufficiently financially prepared for it. Should I rather keep the RA contribution as is with a 5% annual escalation, and look into alternative investments options for purposes of creating an income for that 11-year gap at the end of my official ‘formal’ working life? If so, what investment vehicles would you recommend?

Tristan

I think you said you use your tax refund for tax-free deposit. What about adding it back to your RA each year? Wouldn't that have a cumulative refund benefit? Going into the tax free account means no more instant rewards, you have to wait a decade.

My half-thought out idea is to try hit 27.5% each year, e.g. dump in and top-up any bonuses. My thinking is that it'll be easier in future years because of maxing out my refunds.

The end result should be the same as if my bonus was deposited directly into my RA rather then losing much to tax.

Survivors of a battle with the Debt Monster already got a nasty introduction to the world of fees. A combination of account fees and interest on debt will leave you poorer every time. This baptism of fire may have been unpleasant, but it’s not a lesson you’re soon to forget.

Survivors of a battle with the Debt Monster already got a nasty introduction to the world of fees. A combination of account fees and interest on debt will leave you poorer every time. This baptism of fire may have been unpleasant, but it’s not a lesson you’re soon to forget.

Those most vulnerable to the wealth-destroying effect of fees are those new to the financial world. When you don’t have much money and a brush with debt hasn’t yet alerted you to the grimy side of the financial system, a 1% fee on a small transaction is unlikely to set off alarm bells. On a R300 investment, a 1% is only R3. What could you possibly buy with that? Beware, dear lambs, this is how they get you.

In this week’s episode of The Fat Wallet Show, we try to show you why you should care about fees very much. We run the gamut - from expensive, ego-stroking bank accounts to total investment costs in ETF products.

You might be disappointed to find that we can’t offer cut and dry solutions to fees. A lack of consistency in reporting among financial institutions makes it almost impossible to do a side-by-side comparison of fees. Instead, we try to steer you in the general direction of clarity.

We reference this document.

Kelly

I’ve just received my first salary and am extremely eager to make my first investments into TFSA ETFs, however the more I started thinking about life expenses the more I realised that there are a couple of other financial planning decisions that I still need to make. I would like your advice relating to the following matters:

Which bank account for day to day activities? Investec approached us first year trainees with the young professionals’ private banking account. It has a monthly fee of R295 with no additional charges. It gives you reward points and access to airport lounges and all sorts of shiny bells and whistles.

In what ratio would you advise me to invest my savings into an emergency fund and TSFA ETFs? Also, in which bank account would you advise me to keep this emergency fund?

I am aware of the extreme importance of saving for retirement, and am unsure of whether I should be contributing to a pension fund as well as TFSA ETFs or if focusing only on TFSA ETFs for now will be sufficient. What is your opinion on this?

As I am young, I would like to focus on high risk, high return (hopefully), equity ETFS. I have considered the Satrix Top 40, as it is a known favourite and I can “catch up” on the time I have lost due to the sideways market with the hope of a more favourable market in the near future. I have also considered the Ashburton Global 1200 and Satrix MSCI World ETFs. The new ABSA low volatility ETFs also caught my attention but I am concerned that the risk on these ETFs are too low? Will you please advise?

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

Flipi

Any change in your opinions about 10x as a good RA choice?

Would Stanlib's new TFSA be as good as any other? I have some investments with them and it would be convenient to simply move the money across in the next few days.

Other Gerhard

I opened a TFSA account for each of my daughters and did my first transfer.

I did the instruction on their website and the trade was done 09:15 in the morning.

I bought the Satrix MSCI World ETF and the trade price was R39.16 per share.

From another trading system I use on a personal level I couldn't see this price trade anytime during the day. The highest price traded was R38.65 for the day, which means that over and above the normal small trading fee I paid to EasyEquities I also paid R0.51 or 1.32% of the share price.

I invested R10,000 and the total transaction cost according to their break down was R37.40.

But I got charged R39.16 per share instead of R38.65 (assuming the highest price for the day) and therefore I paid another R130.24 in "transaction charges". The total transaction charges therefore R167.64.

If I did the same size transaction on Investec's trading platform I would have paid R151.72 in charges.

Did I do something wrong here?

Always Abundant

In 2002 we bought into an Executive Redemption bond offered by a UK-based Life Assurance Co via the International arm of a large South African financial institution. This was sold to us by our financial advisor (at the time) as a way to maintain our offshore diversification.

In 2012 we applied for a full withdrawal in order to close the policy. We were able to redeem everything other than 1 of the funds (a UK-based Property fund) which had gone bust. We accepted our losses, which were considerable, and forgot all about it. Recently we received a letter from the International Arm of the local company informing us that the annual fees on the policy had gone up.

I obtained online access to the account and noticed that the Property fund in question had eventually liquidated in 2018. The small amount that was generated from the liquidation had gone towards paying these fixed annual fees. But since the fees were charged continually, there is now in a significant amount owing (1.5K USD).

The policy is worth nothing but the fees continue to accumulate even though we had submitted the withdrawal form years ago. No one has informed us about the fees owing.

What are our rights in this case? Surely there must be some kind of Consumer Protection laws to protect us from being liable for these fees? What should be our course of action, if any?

Win of the week: Phasane

2018/2019 Tax Year has been, surprisingly, a good year for me.

- I finished paying off my car, not planning to buy any car until 2023. The only debt remaining is the bond.

- I discovered the Fat Wallet Podcast and the Just One Lap community in general.

- I listened to all Fat Wallet episodes (the weekly wait is now killing me).

- I moved my RA from Liberty to 10X, a process that started late in October 2018 and about to be wrapped up as I write this mail (waiting for some Trustees what what signature but 10X have kept me informed every step of the way). By the way, I started with my RA contributions to 10X in November and contributed to both Liberty and 10X that month.

- Although I wanted to do more, I contributed 16 600 ZAR to my TFSA (up from the R4 620 that I contributed the previous Tax Year). I am comforted by the fact that I have built my emergency fund to levels I am comfortable, from 0 - 4 months worth of living expenses (in Simon's own words, "that makes me sleep well at night").

2019/2020 goals

- Contribute the max amount to the TFSA, this is important considering TIME in the market.

- Add one more month of living expenses to the emergency fund.

- My normal RA contributions will continue, this is a top up to the work pension fund.

- Everything else remaining, including change from the F##k it monthly budget, goes to the Bond. I am planning to settle the Bond in 2022 (9 years from the registration date)

Tax rebates, bonuses and inheritances really throw us for a loop. Most of us have every cent of our salary allocated to some higher purpose, but the moment we find ourselves with a big hunk of cash, we get in our own heads. We all know what we should do with the money, except because this is magical unicorn money we don’t.

Tax rebates, bonuses and inheritances really throw us for a loop. Most of us have every cent of our salary allocated to some higher purpose, but the moment we find ourselves with a big hunk of cash, we get in our own heads. We all know what we should do with the money, except because this is magical unicorn money we don’t.

We get questions about lump sum investments so often that we decided it’s time to devote an entire episode to it. In short: the math says invest it all at once as soon as possible. If your emotions tell you to do otherwise, however, you should probably pay attention to them first.

We talk about our friend Hendrik’s blog tigersonagoldenleash.co.za in this episode.

Andrew

I just received 10 months worth of salary as a bonus. I currently have money invested in my portfolio. I’m trying to decide how to go about investing my bonus. Should I chuck the entire amount in now? (Keep in mind my TFSA is maxed out for 2018, and I plan on investing R33 000 on 1 March) or should I average it out over a few months? Also keep in mind that I have no debt.

Win of the week: Nadia

I listened to the show about my question and I just want to say thanks a million! You guys helped a lot with my decision and I have decided not to get involved with Forex trading. I first need to focus on my TFSA and make sure I understand all the ETFs I have chosen to invest in.

- Subscribe to our RSS feed here.

- Subscribe or rate us in iTunes.

David

Love the show. I have a question for you relating to picking a Global ETF. I have an Easy Equities Account and have access to investing in ETFs listed on the NYSE.

I was looking at the Vanguard Total World Stock ETF on the USD account and comparing it to the Ashburton 1200 on the ZAR account. The TER is significantly cheaper for the Vanguard ETF – 0.1% vs. 0.45%.

The weighting of the constituents of each ETF are quite similar although the Vanguard has over 8,000 stocks where the Ashburton has over 1,200 stocks which makes it attractive to have more exposure globally.

My feeling is that in the long run, it’s probably worth moving all my investment offshore (into USD) into the Vanguard ETF if I follow the concept of one ETF to rule them all because of the low cost of running the ETF.

What risks other than a strengthen Rand or having a Will in place in the USA to transfer the funds in the event of death would you foresee? How would the tax on dividends / Capital Gains be affected?

Hannes

I recently received a severance package. This money is considered "tax free income" because of a SARS tax directive, which seems to be common with severance packages. It’s been lying in a savings account, and I'd like to know what you think is the most tax-efficient way to put that money to work.

I don't have any investments and no emergency fund. The savings referred to above is currently my emergency fund. The only debt I have is car debt, a monthly expense of R2400. No bond either.

The amount is just enough to max out my TFSA for the 2018 tax year ending in February as well as settle my car debt completely, but then I have no more savings / emergency fund left at all. However I can quickly build up an emergency fund, or to rather contribute aggressively to my car debt with a monthly contribution if I decide to not settle.

It seems crazy dropping a huge amount on my car debt to settle it considering the small monthly repayment, but it's also something I want to get rid of ASAP as it allows for more savings, less essential expenses and more cashflow when I'm rid of the repayment. The risk of course is that I will be stuck without savings / emergency fund for a few months until I can build it up again. I do have a credit card.

Not quite sure what the best course of action is. Should I rather leave the debt as is and invest with this "tax free income"?

Minnaar

I would like to understand how a property-based ETF actually distributes the income that it gets from rentals? How does the ETF distribute this to holders of the product? Is it in the form of a dividend?

Can you explain like I am 5 why some people think investing in REIT properties are a good idea in a TFSA?

Dave

I discovered that you can buy REITSs via unit trusts, exchange traded funds or standalones directly from your stockbroker or financial advisor or a site like EasyEquities. I can see a sort of hierarchy here but just don’t get it. Are earnings from REITs rental income or dividends? I can appreciate that if held in a property owning company the earnings would be in divs. But if held by a unit trust how would rental earnings be paid?

Phil

I love this podcast and this a wonderful public service you're offering to all South Africa.

Even though I'm in the UK and a lot of the advice can't be directly applied the thinking still applies and continues to push my thinking.

I want to share stuff that changed my financial life which was given a wake-up call after I took a massive hit on RA when I financially emigrated and was confronted with just how far behind I was. Painful stuff, and wish I had a podcast like yours to point me in the right direction at the time.

I wanted to share some references I use in the UK that I think would be very useful for reference in your offering to the public as well:

- The go-to reddit (I know, don't take advice from unknown muppets, but it's good) for me is /r/ukpersonalfinance/. In particular I love the UK Personal Finance Flowchart and it's interactive version (which is opensource on github btw...). This flowchart is awesome for visualising where you are on the maturity scale. Super helped my wife with her "O, fok!" moment.

- The second source I love is moneysavingexpert.com. It's a bit of a marketing-hidden-like-advice site, but it's got some gold-level guides on finance basics for people who were never shown how the basics work.

- The more extreme sites are FIRE the based, but drastically shifted my thinking on what retirement means, in particular @firevlondon on twitter is an interesting feed I follow with monevator.com to frame my thinking on passive investment.

Melissa

I already have some investments with Easy Equities, so just decided to move some funds around so that I can put the full R33 000 in for the 2018 tax year.

I am a bit confused about the limit of R33 000 and the fees involved. When I bought my TFSA ETFs the admin/brokerage fees were deducted and my investment amount only shows as R32 877 (R123 admin fee). I know it is a small difference, but I would like to utilise the full R33 000 that I am allowed for the year. Easy equities however does not allow me to invest any more funds into this account.

Do you have any clarity whether this R33k limit includes the administration fees?

André

I heard you say you had to re-open your FNB account because you have and FNB flexi bond.

Not sure what the exact reason is but thought I will share this. You do not need an FNB account to withdraw from your FNB bond. I also have an FNB flexi bond and I nominated an account at a different institution and I have withdrawn from the bond directly into that account.

Fanie

I’m nearly 70 and earn the biggest part of my income from the following ETFs: PREFTX, PTXTEN and STPROP.

You mentioned that because PREFTX consist of many banking pref shares there is a risk should we get downgraded to junk status by all the rating agencies. I understand that a junk grading will affect our total banking system negatively in that interest rates will go up. What do you think will be the effect of a downgrade on my income from PREFTX.

Chris

What stops me from opening a tax free savings account with a overseas fund managers like JP Morgan, Investco, Black Rock etc?

What are the tax implications for me as a non-resident in an international based etf tfsa?

What are the risks and is it something worth investigating?

Conette

I am 55 and work for a big bank group, with lots of good benefits.

My emergency funds sorted out and bond debt almost covered.

I want to open a Tax Free Savings (ETFs) account with Easy Equities .

I please need your assistance in my ETF selection? I intend not to 'touch' the investment in the next 15 to 20 years.

Jo

I am in the process of shifting my RA around and moving away from unit trusts and into ETFs.

I started investing in an RA as soon as I started working, but unfortunately I thought they were very one size fits all and so it's all sitting in unit trusts with fees of around 3.8%.